by Sean

by Sean

The 1 June 2025 disposable vape ban removed one product format from sale, but it didn’t end overall demand for nicotine.

Click here to access the latest Nicotine Products market report.

The customer who was buying a Lost Mary every three days still wanted nicotine on 2 June; they just didn’t know what to buy instead. That demand didn’t disappear, those customers were searching for a replacement product.

The Salience Index shows that the market grew +12.0% in the year the category was outlawed. That growth went to retailers who answered “what do I buy instead?” before their competitors did, and those retailers were often neither the largest nor the cheapest in the market.

Vape UK is a useful example. They added more organic visibility in twelve months than any other brand in the top 100 of the 304-brand dataset. Their product range stayed broadly the same; what changed was their navigation.

The numbers

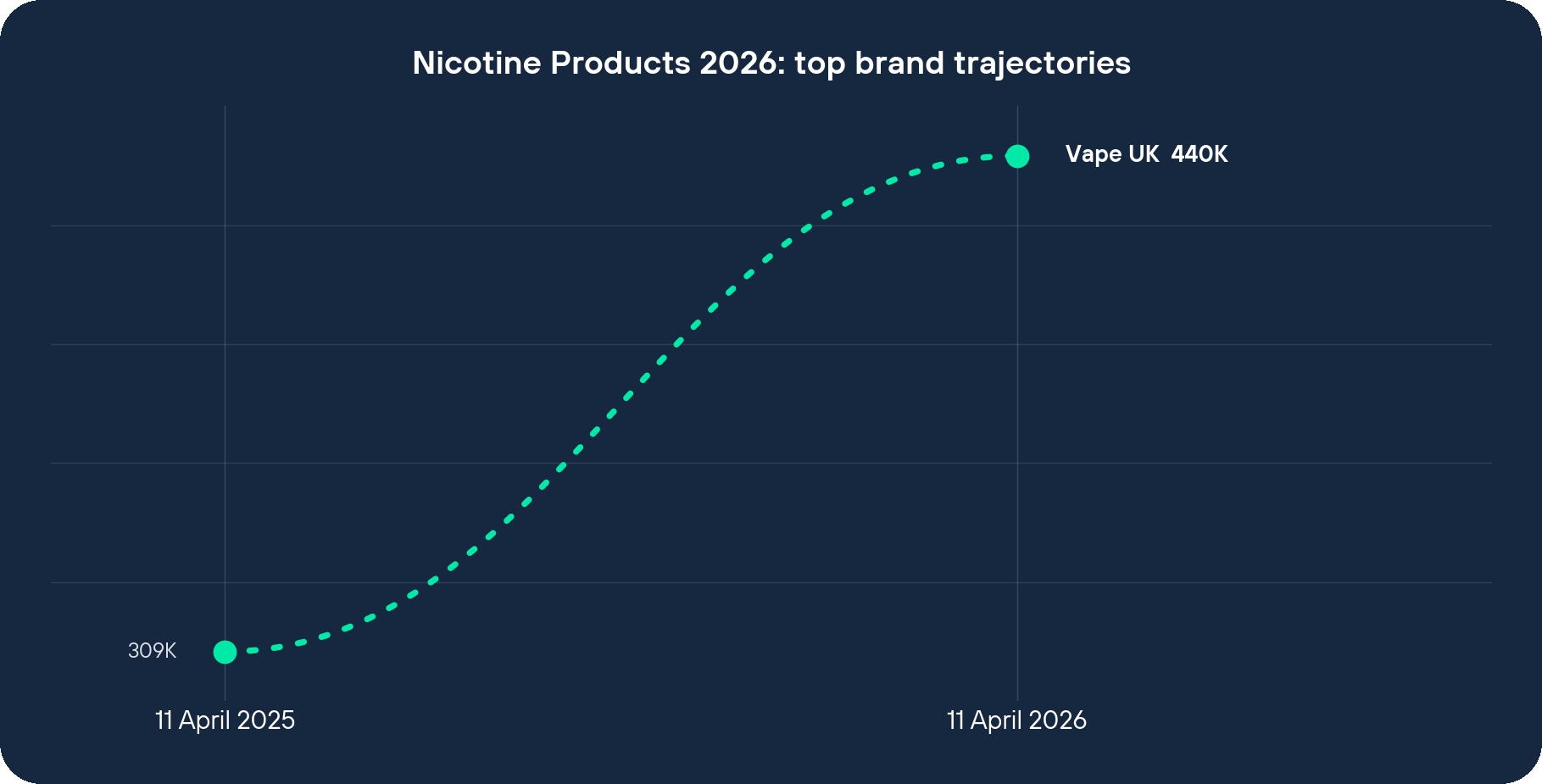

Vape UK went from 308,998 to 439,519 visibility between 11 April 2025 and 11 April 2026. That’s an absolute gain of +130,521, or +42.24% year on year against a market growing +12.0%, roughly 3.5× the category baseline.

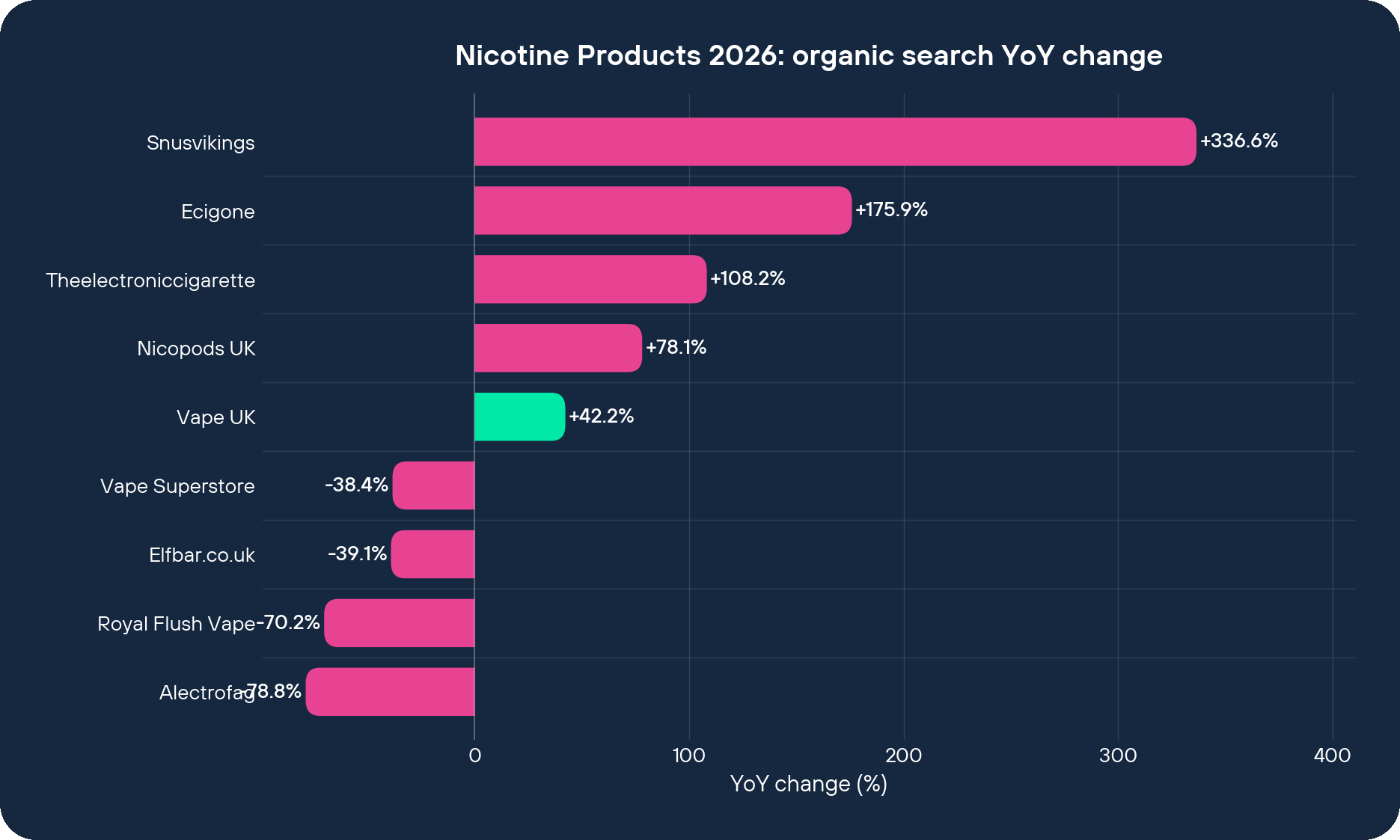

It’s the largest absolute gain in the top 100.

Vape Superstore makes the contrast clear. Same retailer model, same independent specialist positioning, the same Vaporesso promo running on the homepage, and more reviews, 33,975 5-star against Vape UK’s 15,341, yet it lost 99,873 visibility, down 38.35%, the single biggest absolute loss in the dataset.

And it’s not just these two. Snusvikings (+336.55%), Ecigone (+175.88%) and Theelectroniccigarette (+108.23%), refillable-first sites and pouch challengers posting double and triple-digit growth, while Elfbar.co.uk dropped -39.07%, Alectrofag -78.83% and Royal Flush Vape -70.22%. The brands whose homepage was built around a now-illegal product format lost ground sharply.

The redistribution is real. The question is what Vape UK did that Vape Superstore didn’t.

The bet

The bet is small. Almost embarrassing in how small it is. They made “Disposable Alternatives” one of seven top-level navigation categories.

They made it a primary navigation item, sitting next to “E-Liquids” and “Vape Kits”, rather than treating it as a campaign page, a banner or a blog post.

That’s the decision. Treat the customer’s new question, “what do I buy now my Elfbar is gone?”, as a first-class category, equal weight to the product types that have been first-class for fifteen years.

What it costs: brand-loyal disposable shoppers see “Alternatives” and feel managed. They wanted continuity. You’re flagging discontinuity. Some bounce.

What it protects: every search query that includes “instead of”, “replacement for”, “best after disposables”, “refillable like Elfbar”. That’s the entire net-new demand the ban created. Every retailer is competing for those queries. Vape UK is the only one whose top-level IA matches the query’s vocabulary.

A banner or a promo can’t deliver that; it has to live in the navigation, because the navigation is the first thing the page renders and the first thing Google parses.

What the two homepages do differently

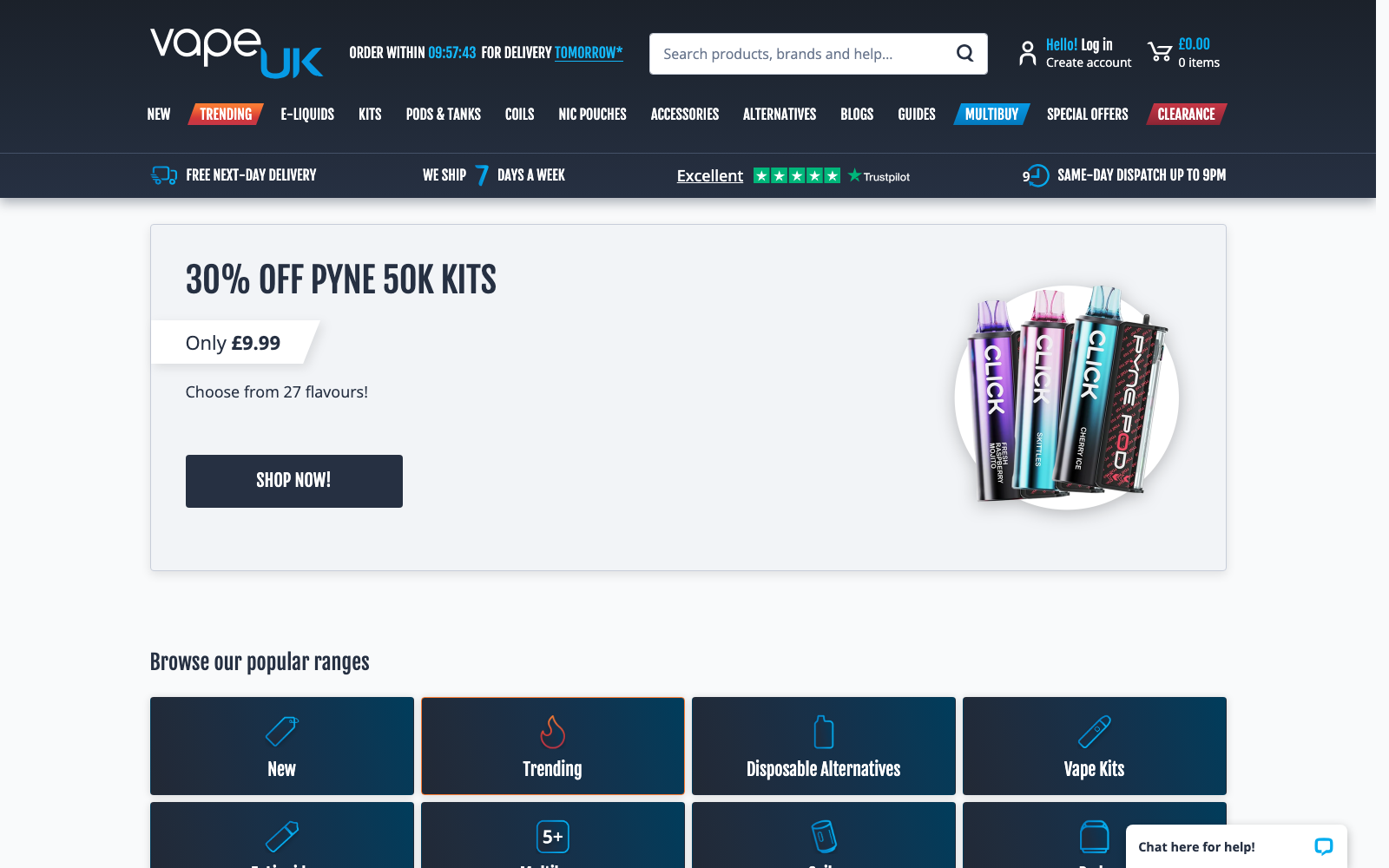

Vape UK’s top nav: E-Liquids, Vape Kits, Prefilled Pods, Vape Coils, Nicotine Pouches, Heated Tobacco, Disposable Alternatives. Seven categories. The seventh is the new one.

Hero unit: “Free Dojoliq with all refillable Vaporesso kits from only £9.99.” A Vaporesso refillable pod kit at £9.99, roughly two days of a £6-£8 disposable habit. The kit is bundled with free e-liquid, which removes the second-purchase objection that kills disposable-to-refillable conversion (“I bought the kit, now I have to figure out which liquid?”).

The price point matters. £9.99 is an impulse number, closer to the cost of dinner than to investing in a new system.

Trust signals: free next-day delivery on £20+, same-day dispatch to 9pm seven days a week, established 2016, a prominent reviews badge. None of these are unique to Vape UK, but all of them are necessary.

Vape Superstore runs the same Vaporesso Dojoliq promo and the same delivery promise (“Free Next Day Delivery, Orders over £20”, “Up to 10PM, Same Day Dispatch”), and it has more reviews at 33,975. The assets are there.

Its navigation, though, lists six categories: E-Liquids, Vape Kits, Prefilled Pods, Vape Coils, Nicotine Pouches, Heated Tobacco. There is no seventh.

Its trending shelf shows Bar Juice 5000 Nic Salts and Vampire Vape 10K Prefilled Pods, bar-shaped continuity products. The “10K” in a product name is the tell: it’s a disposable’s puff count, repurposed as a prefilled pod. Vape Superstore is trying to keep the disposable customer in the disposable mental model.

The Vaporesso refillable promo is on the homepage, but it sits as a banner on top of a disposable-era category structure. The navigation itself didn’t change.

Cost of that difference: -99,873 visibility.

What this means for everyone else

Every retailer in the dataset had the same information on 1 June 2025. They all knew the ban was coming, it had been legislated for months. They all had Vaporesso in their catalogue, and they all stocked pouches, refillables and prefilled pods. The same supplier guidance reached everyone at the same time.

What separated the winners from the losers came down to a single navigation decision: whether you treated “what do I buy instead?” as a top-level question or buried it. Product, price, delivery and reviews were broadly the same across the field.

That should change how you think about category structure.

Stop treating your navigation as a static map of your catalogue. Treat it as the first answer you give to the customer’s current question. If the question changed, and a category-wide product ban is the most binary version of “the question changed” you’ll ever see, your navigation has to change.

The common mistake is to bolt a banner onto the old taxonomy. The promo says “we have refillables” while the navigation still says “we sell disposables, mostly”, and the navigation wins because it’s what Google reads.

The pouch story is the other half of this. Snusvikings (+336.55%), Nicopods UK (+78.08%) and Ecigone (+175.88%) won net-new search demand that didn’t exist when disposables were the default nicotine product. The customers moving to pouches show a different intent, “nicotine without vapour”, rather than ex-vapers continuing the same habit. Retailers with pouch-forward navigation captured that demand; retailers with pouches buried two clicks deep did not.

If you sell anything where consumer behaviour has just shifted, and most categories have something shifting, your navigation is the conversion strategy that matters most, ahead of the hero unit or the bundle. The top-level categories are what to get right.

What we can’t say from this data

The Salience Index measures organic visibility rather than revenue. Vape UK could be ranking for higher-volume, lower-commercial-intent queries. We don’t see their conversion rate or their margin on a £9.99 kit. Their +42.24% organic growth might come with a softer average order value, we can’t tell from this data.

And the broader redistribution thesis holds at market level (+12.0%) but individual brands inside it might be losing margin even while gaining visibility.

To summarise: when a category is banned, the retailers that rebuild their navigation around the customer’s new question gain visibility share, and the retailers that bolt a promo onto the old category structure lose it. Vape UK gained +130,521 visibility and Vape Superstore lost 99,873 over the same twelve months, both running the same Vaporesso promo. The difference came from navigation decisions.

If you want the underlying numbers, all 304 brands, every category movement, the redistribution mapped out, they’re in the full 2025 Nicotine Products report. And if you’re trying to capture the “instead of” and “replacement for” queries the ban created, you’ll need content that answers replacement-intent queries sitting behind the nav change.

Further reading

- ecommerce SEO and category structure, The article argues that top-level navigation decides who wins post-ban redistribution, so a reader will want help auditing category structure and faceted navigation on their own site.

- how trust signals convert vape shoppers, Vape UK’s homepage leans on reviews, delivery promises and bundled offers to convert disposable refugees, and this piece breaks down why those credibility cues matter on page one.

- 2025 nicotine industry analysis, Gives the reader the wider sector backdrop, pouch growth, refillable migration, post-ban winners and losers, that sits behind the Vape UK case study.

- 2025 Alcohol industry report, Alcohol retailers face the same regulated-category dynamics, restricted advertising, shifting consumer intent, supplier-led promo cycles, so the parallel sector report is a useful adjacent read.