by Sean

by Sean

The Moment Brand Equity Stops Working

Click here to access the latest Confectionery market report.

A market that fell -36.00% year-on-year should be a horror story for everyone inside it. It mostly is. But the brands that got hurt worst are not the ones with weak names, they are the ones with strong names and nothing else.

The assumption, quietly held across most marketing teams, is that brand familiarity translates into search presence. People know the brand, therefore they search for it, therefore it ranks. It is a reasonable theory. The data does not support it.

Across a 245-brand dataset tracking organic traffic from February 2025 to February 2026, the brands losing most ground are frequently the ones you would recognise in a supermarket aisle. Famous is not the same as findable. Recognition is not the same as relevance to a search query at a specific moment in a buying journey. Google does not rank names. It ranks content that answers intent.

Lindt is a useful example of what the alternative looks like.

Evidence

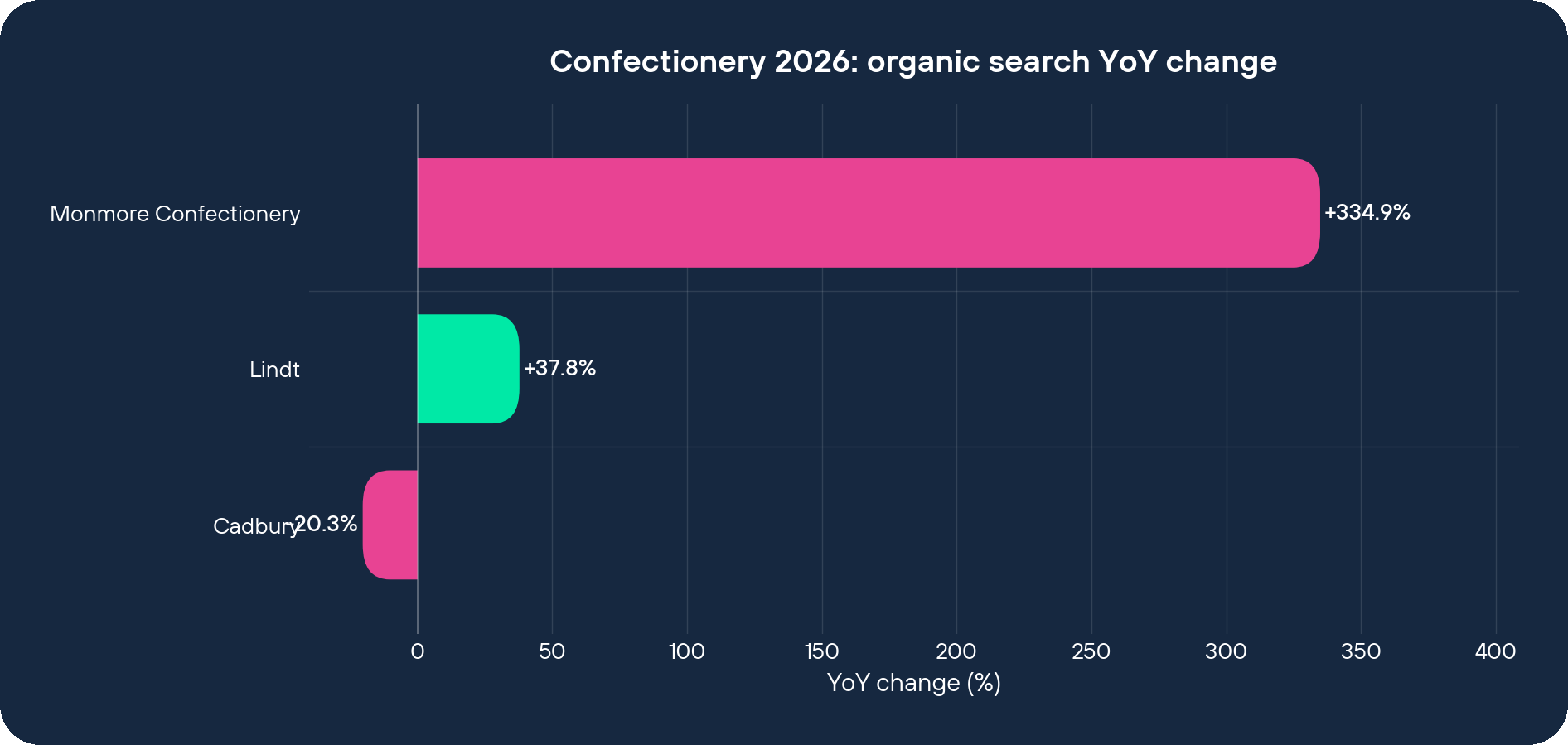

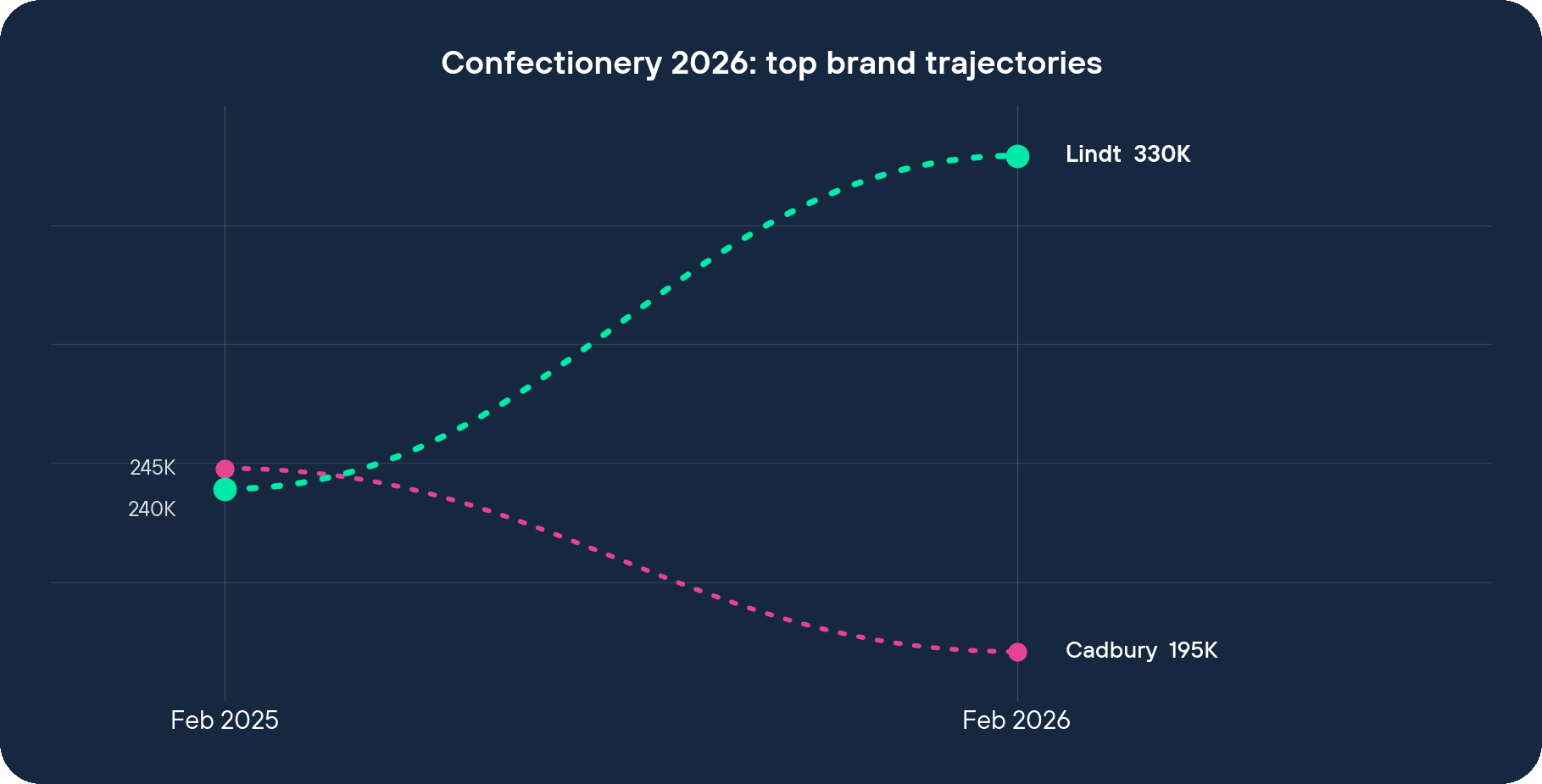

The numbers are not subtle. In February 2025, Lindt attracted 239,773 organic visits to lindt.co.uk. By February 2026, that figure had reached 330,466, a gain of 90,693 visits, up +37.82% year-on-year. Against a category that contracted by -36.00% over the same period, Lindt’s outperformance margin was +73.82 percentage points. That is the largest absolute positive gain among the top ten trafficked brands in the dataset, and it is enough to place Lindt at traffic rank 2 across all 245 brands.

For context: Cadbury, BRS rank 5, 90,500 monthly brand searches, one of the most recognised names in British confectionery, ran the opposite direction. cadbury.co.uk went from 245,362 visits to 195,492, a loss of 49,870 visits, down -20.33%. Traffic rank 5. In February 2025, Cadbury was ahead of Lindt by 5,589 visits. By February 2026, Lindt had opened a 134,974-visit lead. The net swing over twelve months: +140,563 visits, from behind to dominant.

Lindt’s Brand Reach Score rank is 2 with 49,500 monthly brand searches, meaningfully lower name recognition than Cadbury. Its review profile sits at 4,591 reviews and 4.2 stars, placing it at review rank 15. There is nothing in the authority or reputation data that explains a gap of this size.

The gap that opened between these two brands is a strategic gap, not a brand equity gap.

The Decision

The one deliberate bet Lindt has made is this: treat the website as a continuously publishing seasonal and product content operation, not as a product catalogue with a homepage wrapper.

Most teams avoid this because it is expensive and unglamorous. It requires editorial discipline that has nothing to do with a campaign calendar. Someone has to decide, months in advance, that Cherry Blossom Sakura and Strawberry Matcha are the spring editorial story. That Easter gets a spend-threshold promotional mechanic. That Pick & Mix as a format needs its own seasonal refresh and its own SKU family, not just a filter on the existing range. It requires a content team that is permanently in-cycle rather than project-by-project.

What it costs is real. Persistent editorial resource. Tight coordination between product development and content planning. A willingness to rotate the homepage before the previous seasonal story has finished performing.

What it protects is the compounding logic. Every time Lindt publishes a gifting price tier, it creates a permanent search entry point for a discrete purchase intent. Every new product that gets front-page editorial treatment acquires backlinks, internal links, and indexed content that keeps working after the launch window closes. A competition ends. A gifting architecture does not. The difference between Lindt and Cadbury is not that Lindt works harder. It is that Lindt builds assets that compound, and Cadbury builds engagement moments that expire.

The Walkthrough

Visit lindt.co.uk and nothing is static. The homepage is in editorial mode: the Tokyo Style Japan launch, Cherry Blossom Sakura, Strawberry Matcha, gets the kind of front-page treatment usually reserved for Christmas collections. The Easter Sale carries spend-threshold promotional mechanics. Spring Pick & Mix is its own product family, not a filtered view of existing range. The Dubai Style and Pistachio Dark bars are front-page editorial items. None of this looks like it was built by the same team that manages the product database.

The gifting architecture is the structural engine underneath all of it. Gift Hampers, Gift Bundles, Excellence bar, Pick & Mix Selection Boxes, across price points of £24, £33, £42, and £95, each serving a different search intent cluster. The person searching “chocolate gift under £30” lands somewhere different from the person searching “luxury chocolate hamper.” Lindt has built the architecture to capture both, and a dozen intents in between. None of those pages go dark after Valentine’s Day. They sit in Google’s index permanently, accumulating authority, waiting for the next search.

Product innovation is surfaced as content, not buried in catalogue. The Pick & Mix Flower Tin 600g and the Jumbo 2kg are not listed products, they have editorial presence at the moment a new search intent cluster is forming around the format. The product exists. The content exists. The search opportunity gets captured before the competition has finished stocking the SKU.

Now visit cadbury.co.uk. There is real investment here. A recipe hub. Fan-submitted UGC recipes. A Win For Your Squad competition with football icons and matchday tickets. A £100K cash prize mechanic. A Bournville relaunch with chopped hazelnut and salted caramel and genuine editorial attention. These are not low-effort assets. But the structure is campaign logic, not compounding architecture.

The Win For Your Squad competition ends. The cash prize mechanic closes on a date printed on the pack. The recipes accumulate, but they are anchored to Cadbury as a baking ingredient, not to Cadbury as a gifting destination. When the competition window closes, the traffic spike that came with it closes too. Cadbury is generating engagement moments and converting brand affinity into short-cycle traffic. That is a real strategy. The data suggests it is a less durable one.

Cadbury’s traffic rank is 5 out of 245 brands. It is not collapsing. But it shed 49,870 visits in twelve months and is now 134,974 behind a brand that fewer people search for by name.

Implications

If Lindt is winning because of a content architecture decision, the uncomfortable question for every other brand in this market is: what are we building that compounds?

Most confectionery brands have content. Almost none of them have content structured around search intent at every stage of a seasonal gifting journey. The recipe hub, the competition, the social integration, these are brand touchpoints that work for awareness. They do not work for the person who has already decided to buy chocolate and is now trying to decide what, from whom, at what price point. That person goes to Google. If the brand hasn’t built architecture around that moment, tiered gifting, evergreen product editorial, seasonal entry points that stay indexed year-round, then it is invisible at the exact moment the sale is closest.

The category fell -36.00%. Within that declining category, the brands gaining ground are the ones that gave Google something permanent to index and serve. Monmore Confectionery grew +334.88% in the same period. Neither result is a coincidence. Both reflect an organic search presence that was actively constructed rather than passively assumed.

The reframe for any marketing team sitting in this category is mechanical: gifting architecture is a search strategy. Price tiers are keyword clusters. Product launch editorial is link acquisition. Seasonal content rotation is not calendar management, it is compounding organic asset creation. The question to stop asking is “what’s the campaign?” The question to start asking is “what’s still working in eighteen months?”

The brands that don’t make this shift are not going to collapse overnight. They are just going to keep watching brands with smaller names, lower social scores, and less above-the-line spend gradually own more of the searches that convert.