by Sean

by Sean

A footwear market down 12% and the average retailer just absorbed it

Click here to access the latest Footwear market report.

A market shrank -12.0% in twelve months and the average retailer just absorbed it.

That’s the real story behind the Footwear Salience Index. 260 brands walking into the same headwind. Most of them quietly bleeding traffic. Telling themselves it’s the category. “Everyone’s down. It’s the cost of living. People aren’t buying shoes.” Sure.

But “everyone’s down” is a story executives tell themselves to avoid the more uncomfortable one. The market doesn’t make decisions. Brands do. And inside every aggregate decline is a winner consuming the losers’ future demand at a rate that won’t show up in this quarter’s board pack but will look obvious a year from now.

That’s why Schuh is a useful example. Not a hero. Not a case study. Just the brand whose decisions, against an identical headwind, are easiest to read in the data.

What the Salience Index shows across 260 footwear domains

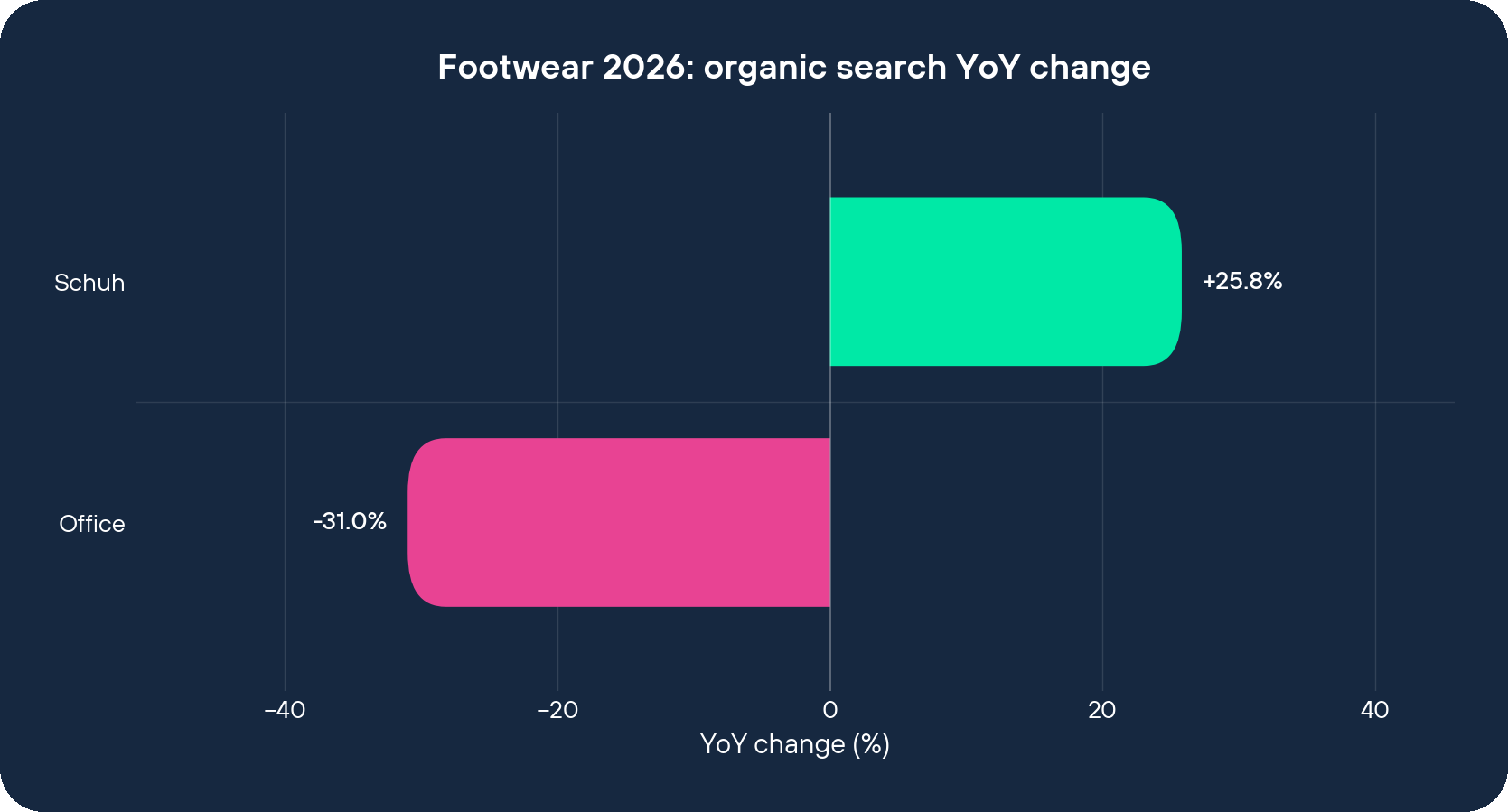

Here’s what the Salience Index shows, March 2025 to March 2026.

The category lost -12.00% aggregate traffic across 260 footwear domains. Schuh.co.uk gained +467,557 monthly visits, a +25.81% YoY rise, which puts it 37.81 percentage points above the market. Office.co.uk lost -532,175 monthly visits, a -30.99% drop, 18.99 points below it. The combined swing between two near-identical retailers is 999,732 visits in twelve months.

Twelve months ago the gap between them was 94,405 visits, a 5.5% margin, functionally a dead heat. Today it’s 1,094,137 visits, a 92.3% structural lead. The delta between the deltas is 999,732 visits of distance manufactured in one year, in the same market, selling the same products to the same customers.

That’s the traffic table. The brand-search table tells you why.

Schuh sits at Brand Reach Score rank 17 of 50, with 823,000 monthly branded searches, social rank 27. Office sits at Brand Reach Score rank 26, with 201,000, social rank 31. Roughly a quarter of Schuh’s brand demand. Nine places apart in the awareness layer. Four-times-multiple in monthly searches. Neither retailer makes the top 20 by review volume, so this isn’t a trust-signal story.

It’s a demand-creation story. Schuh has been buying mindshare. Office has been waiting for it.

The bet: investing in branded demand while the market shrinks

Now, the bet.

Schuh has decided that in a declining market, the only worthwhile investment is in branded demand. That sounds obvious until you notice what it costs. Brand search is the slowest, most expensive, least attributable line on the marketing roster. It’s the budget that gets cut first when the CFO sees a -12.00% category trend and asks “where can we save?”

There’s a reason for that. Because brand search doesn’t move quarterly numbers. It moves twelve-month numbers. It compounds. And it can’t be switched back on quickly once it’s been switched off.

I’ve put myself on a tangent here, but stay with me. The annual budget cycle is what’s actually driving most retail marketing decisions. Not the customer. Not the competitor. The CFO’s spreadsheet, which evaluates spend monthly, demands payback inside the fiscal year, and treats brand investment as discretionary because nobody in the room can attribute it. So the brand line gets trimmed. The performance line gets defended. The trim looks prudent on the spreadsheet and, twelve months later, looks like a cliff in the search data. Anyway, back to the point.

Schuh’s bet, I can’t see the boardroom, but the data smells exactly like this, is that the market correction is a permission slip. While everyone else cuts to protect margin, Schuh has held the brand layer steady or pushed harder. The -12.00% gives them cover. They look like they’re “managing through the cycle” while actually absorbing the demand the cutters are giving up.

What that bet protects: a structural traffic moat that makes acquisition cheaper for the next decade. What it costs: this quarter’s EBITDA. Most retailers won’t take that trade. Schuh did.

How the branded-shoe search moat plays out in the data

Here’s how the bet plays out in the search data.

Schuh sits at traffic rank 5 across all 260 footwear domains. One rank behind Adidas. Ahead of New Balance, Office, Asics, every UK multi-brand competitor in the cluster. That’s a strange place for a UK-only retailer to be. Schuh got there because it converts a slice of every branded-shoe search into a “Schuh has it” landing, when somebody Googles “ASICS Gel-1130”, “New Balance 530”, “Nike Dunks UK”, the multi-brand retailer that’s invested in PDP visibility shows up. That’s the moat. It’s a moat made of other people’s brand demand.

Office’s authority shape is the opposite. Office is at traffic rank 7, only two ranks behind Schuh, but at Brand Reach Score 26, nine places behind. Translation: when people search for shoes, Office still ranks. When people search for Office, fewer of them do it. The traffic is borrowed from the category, not owned in the brand. “We’re still in the top ten” is a true sentence and a misleading one.

That’s a fragile position. It works while the category is growing. It collapses when the category shrinks. Because the retailers with the brand-search base hold their floor. The retailers without it lose air at exactly the rate the category does, plus their own under-investment.

Look at the cluster Schuh is competing in. Sports Direct: traffic rank 1, Brand Reach Score 5, 4,090,000 monthly branded searches. JD Sports: traffic rank 3, Brand Reach Score 4, 2,740,000. Nike: traffic rank 2, Brand Reach Score 1, 1,500,000. The retailers with the largest traffic floors all have correspondingly enormous brand-demand bases. Schuh, with 823,000 branded searches, is the smallest of that cluster. But it’s the one growing its visit count fastest among them, +25.81% in a market down -12.00%. Office, at 201,000 branded searches, is in a different weight class entirely, and it’s the one losing weight.

Now imagine you’re sitting in Office’s planning meeting, looking at last year’s numbers. The instinct is “double down on category.” Run more discount media. Push more acquisition. Win the deal-hunter. “Let’s get aggressive on price.” That sounds rational. It’s the move most teams will make. And it’s exactly what hands Schuh the next million visits.

Now flip that on its head. Imagine the same meeting at Schuh. Same -12.00% headwind. Same investor pressure. The instinct that wins isn’t “cut to match the market.” It’s “the market is shrinking, so the next pound of mindshare is cheaper than it’s been in five years.” Different room, different decision, identical inputs.

What this means for any footwear brand that recognises itself as the Office

So here’s what this means for any retailer reading the Index and recognising themselves as the Office in their category.

The category doesn’t decide the outcome. The brand-search base does. If your branded demand is small and your traffic is borrowed from category keywords, a market correction won’t just trim you, it will accelerate the structural gap with whoever invested in mindshare while you were polishing CAC.

That changes the job. Most retail marketing teams are organised around “performance” and “brand” as separate budgets, with separate KPIs, judged on different timescales. The Schuh-Office data says that structure is the problem. Brand search isn’t the brand team’s deliverable. It’s the only durable input into the performance team’s CAC, twelve to eighteen months out. Treating them as separate lines is what makes the brand line cuttable when it shouldn’t be.

The very fact that nobody is ever fired for under-investing in brand search, because the metric has no quarterly visibility, is exactly why most teams under-invest in it. It’s a credit/blame asymmetry. Cutting brand spend in a downturn is “prudent.” Holding it is “extravagant.” Until the market turns and your CAC has tripled because you no longer have a brand demand floor to cushion it. By that point the executive who made the prudent cut has been promoted, and somebody else is wondering why the funnel is broken.

What becomes first-class? Monthly branded search volume as a tracked, reported, defended metric. Treated as a leading indicator of next year’s traffic floor.

What stops being first-class? Quarterly ROAS on category keywords as the dominant marketing scorecard.

What the search data can’t tell you

The Salience Index measures organic search visibility. It doesn’t see paid spend, app installs, retail footfall, email revenue, or wholesale trade. Schuh might be running paid that explains some of this. Office might have a repositioning underway that won’t show up in search for two more cycles. The honest version is narrower: the search outcome is what the data shows.

But the search outcome is a leading indicator of the rest. Which is why, in a declining market, the brand still buying mindshare isn’t growing through luck, it’s consuming everyone else’s future demand.

Stay human,

Sean