by Sean

by SeanPeople don’t search “pet shop” anymore. They search “fluralaner for dogs 20kg” at 11pm with a worried face and an open vet tab. They search “advocate for cats”. They search “yumove for senior hip joints”. The retailer used to be the unit of demand. It isn’t anymore. The condition is. The medication is. The species-plus-problem is. So the brand that wins isn’t the one with the biggest sign over the door. It’s the one whose top nav looks the way a worried owner actually types.

Click here to access the latest Pet Supplies market report.

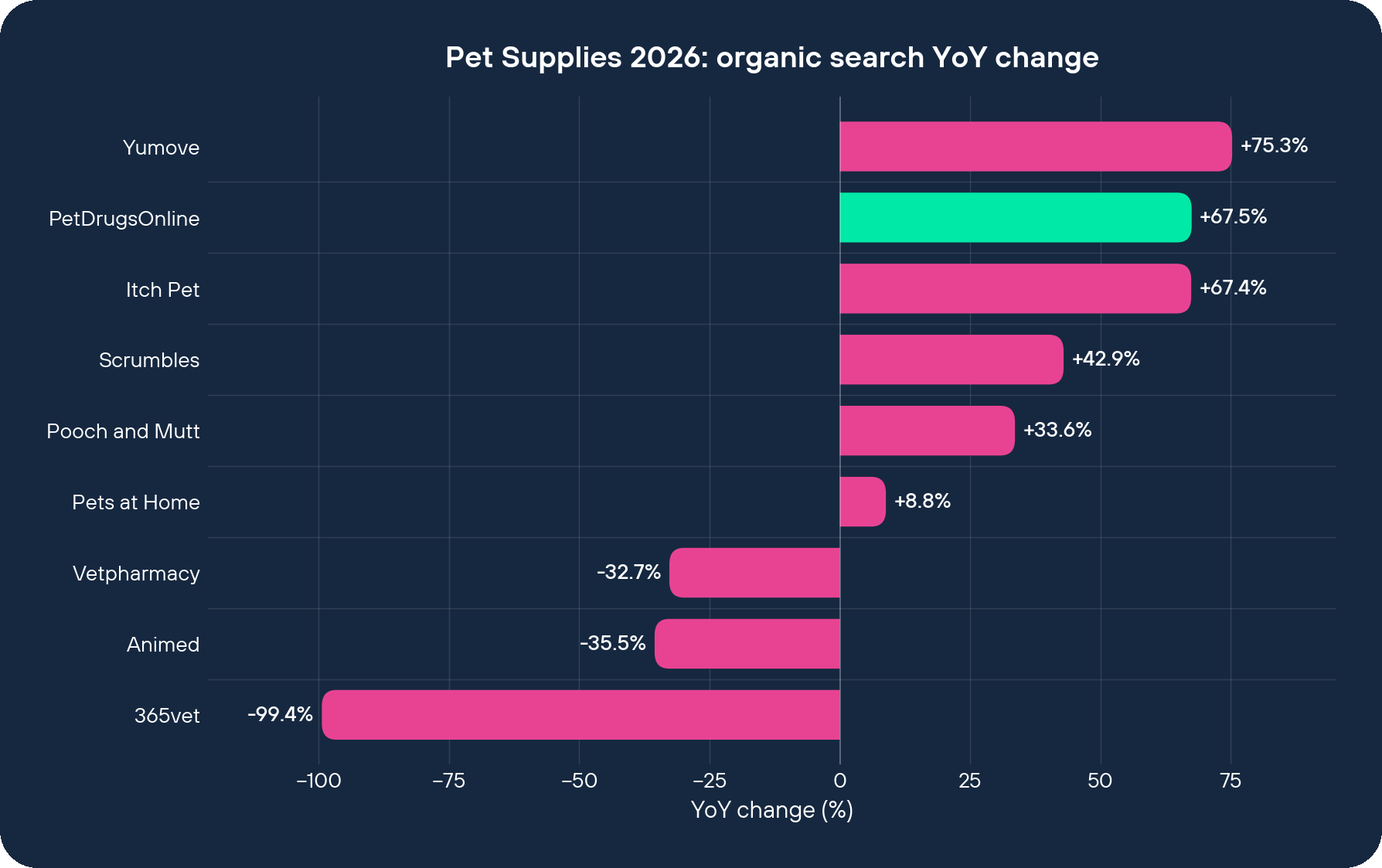

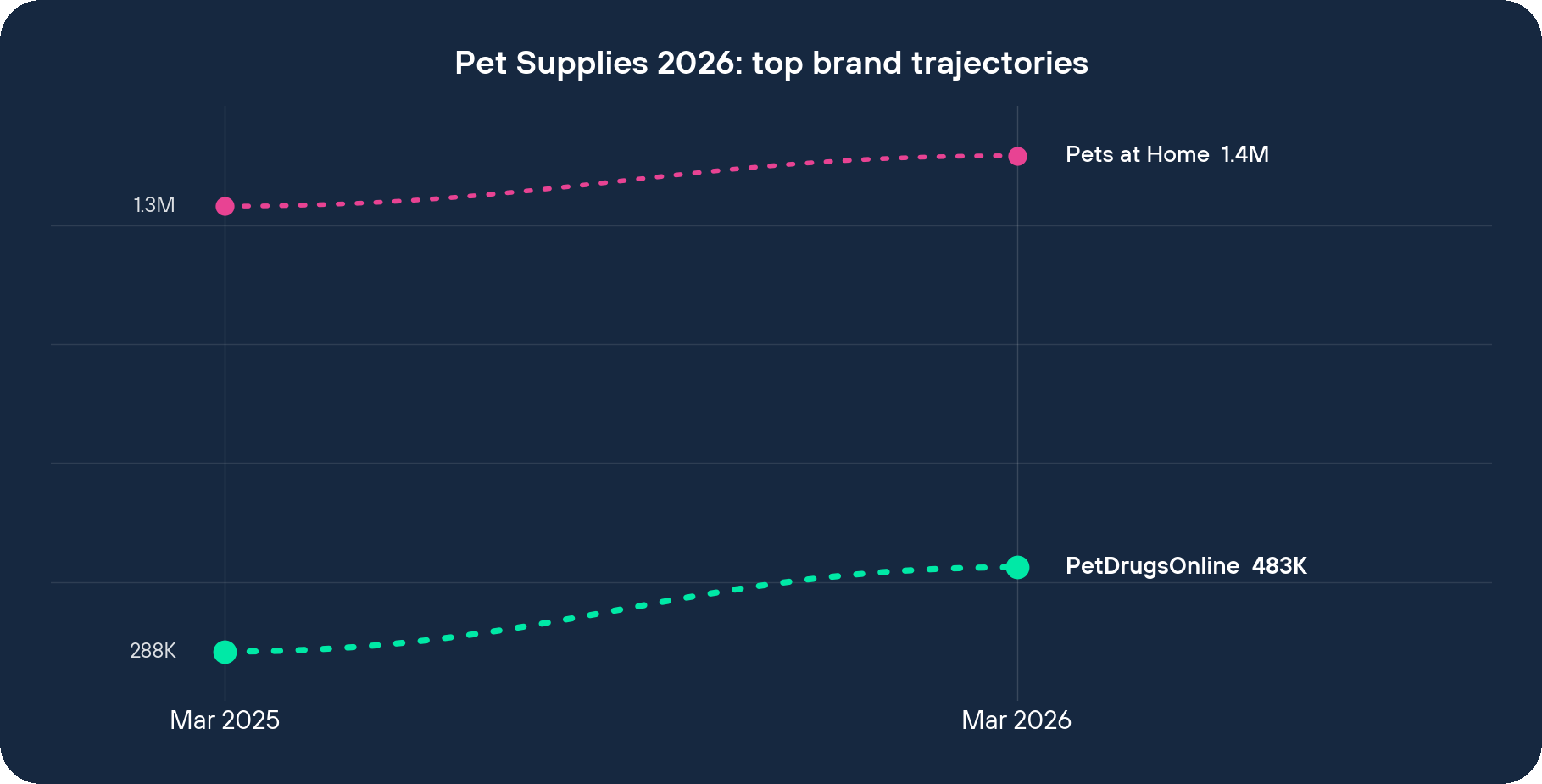

PetDrugsOnline is a useful example of that. Not because they’re cool. Not because they’re famous. Because they grew +194,616 organic visits in twelve months on a base of 288,340, while Pets at Home, sitting on 1.5 million monthly brand searches, added +116,240 visits on a base of 1,316,834. Smaller brand. More absolute growth. 7.6 times the YoY percentage. There’s a reason for that.

Evidence

The numbers are uncomfortable for the household name.

PetDrugsOnline: 288,340 to 482,956 organic visits between March 2025 and March 2026. +67.50% YoY. The pet supplies category grew +14.00% over the same window. So they’re running 4.8x the market and 7.6x Pets at Home’s +8.83%.

Pets at Home: 1,316,834 to 1,433,074. +8.83%. That’s 5.17 percentage points below the market. Brand Reach rank 1. Brand-search rank 1 with 1.5 million monthly searches. Adding traffic in absolute terms, yes. Losing relative share, also yes.

Now look at the rest of the table. Yumove +75.27%, +61,891 visits. Joint-supplement specialist. Scrumbles +42.93%, +18,212 visits. Sensitive-gut food specialist. Itch Pet +67.42%, +9,737 visits. Subscription parasite treatment. Pooch and Mutt +33.60%, +35,818 visits. Functional dog food.

Now look at the other side of the column. Animed minus 54,486 visits at minus 35.54%. 365vet minus 37,846 at minus 99.39%. Vetpharmacy minus 6,362 at minus 32.71%. The horizontal vet-supplies catalogues are getting eaten.

The pattern doesn’t fit “Pets at Home is dying.” Pets at Home is fine. The pattern fits “the catalogue retailer is fine, the catalogue specialist is winning, and the unit of demand has changed underneath all of them.”

PetDrugsOnline doesn’t even rank loudly. Brand Reach rank 8. Social rank 27 of 50. 110,000 monthly brand searches against Pets at Home’s 1.5 million. They aren’t winning by shouting. They’re winning by being the answer to a question Pets at Home isn’t structured to answer.

Decision

Here’s the one bet they made. Organise the site around the job, not the species.

That sounds obvious. It isn’t. Every retail merchandiser instinct screams “shop by pet” because that’s how the catalogue is structured, that’s how the warehouse is structured, that’s how the buying team is structured. Dog buyer. Cat buyer. Small animal buyer. The whole org chart says species. So the IA says species. So Google sees species. So you rank for “dog food brands” and you don’t rank for “apoquel 16mg”.

PetDrugsOnline ignored all of that. Their top nav is Prescription Medication, Flea/Tick/Worming, Subscriptions, Prescription Information. Four of seven slots are condition and medication intent. Not “Dog”. Not “Cat”. The job comes first.

The cost: they can’t be the friendly local pet shop. A first-time hamster owner won’t land there. The dad buying a Saturday treat won’t land there. They’ve given up the top of the funnel.

What it protects: every 11pm vet-referral query. Every parasite refill. Every “what does my vet mean by fluralaner”. That’s where the volume now lives. And that’s where they’ve parked the whole house.

Walkthrough

Land on petdrugsonline.co.uk and the homepage is a workflow, not a window display.

Four steps across the top. Search Prescription Meds. Ask Your Vet. Find Your Pet’s Medication. Upload A Photograph Of Your Whole Prescription. Read that again. That is not a hero banner. That is a transactional flow. The page is telling you: “you came here with a job, here is the job, here are the four steps to do the job.”

Below that, tabbed product modules. Best Sellers. Pet Food. Flea & Worming. Hard SKU lists. SKU 1982. SKU 2282. SKU 2284. That’s not merchandising. That’s an inventory rack tuned to product-type and active-ingredient queries. Google sees the SKUs and the ingredient names and the body content. It indexes the whole stack.

Then the trust furniture. 650 brands stocked. 192,000 reviews. 20 years of service. That’s not lifestyle copy. That’s authority parked exactly where Google now demands it for medication queries. They’re answering the same YMYL signal demands you’d answer on a human pharmacy site.

Now Pets at Home. Open petsathome.com. The hero is “Pets Club Prices.” The next module is “Shop by Dog / Cat / Small Animal / Fish / Reptile / Bird.” Then “Pets Talk: advice and inspiration”, feeding kittens, feeding puppies, “Bringing a new kitten home is exciting”. Then the loyalty programme benefits. Birthday treats. Charity Lifelines. Free Pets magazine. A vet health check for £10.

It is a beautiful pet-parent lifestyle site. It does the brand job. It does the loyalty job. It is, by any measure, a serious piece of CX. It just isn’t designed for the query “fluralaner 1360mg dog”. And the query is where the volume went.

Look. Six species tiles. Zero condition entry points above the fold. The IA was set when the IA was right. The IA is now wrong.

Implications

Now imagine the head of e-comm at a generalist proposing this in the Monday planning meeting. “I want to tear up nav and rebuild around condition.” There’s a reason that idea dies in the room.

The merchandisers can’t restructure their feeds. The buyers are organised by species, not condition. The legacy URL structure can’t be broken without an SEO discussion. The loyalty programme is the strategic asset. The CRM segmentations are by pet type. Everything in the building is set up for “shop by pet”. The very fact that you’d suggest “shop by condition” exposes you to a six-month war with seven internal stakeholders. People don’t get fired for re-skinning the dog food page. They get fired for breaking the IA.

So the IA stays. The specialist eats.

I’ve put myself on a tangent here, but stay with me. Think about how humans search for their own medications. We don’t type “Boots, please find me something for a headache”. We type “ibuprofen 400mg” or “co-codamol side effects”. The pharmacy isn’t the unit of demand, the drug is. The reason I’m telling you this is that pet owners now do the same thing online, and there’s nothing keeping condition queries trapped inside a species nav.

Back to the point. Now flip that scenario on its head. Imagine the head of e-comm at PetDrugsOnline in 2005. They didn’t have a species nav to defend. They didn’t have seven stakeholders. They had a prescription form, and they built the whole house around it. Twenty years and 192,000 reviews later, that house ranks for every condition query Google rewards. The advantage compounds quietly because nobody had to fight for it.

If the unit of demand is the condition, three things break in the generalist playbook.

The hero shelf is wrong. It’s species. It should be intent.

The category hierarchy is wrong. It’s “Dog Food, then sub-type”. It should be “Condition, then species, then product”.

The loyalty programme isn’t where the volume gap is. The gap is in 11pm queries that loyalty members don’t even attribute back to a generalist brand.

A senior reader will object: “But Pets at Home is still rank 1 by Brand Reach.” Sure. Brand strength buys you the search-for-the-shop traffic. It doesn’t buy you the search-for-the-thing-inside-the-shop traffic. The second one is now bigger than the first, and growing faster.

Guardrails

This is organic-search data only. We don’t see paid. We don’t see basket size. We don’t see margin. PetDrugsOnline could be winning the wrong customers, low-margin prescription refills with thin baskets, while Pets at Home prints money quietly on accessories and food subscriptions. Their Trustpilot rating sits at 4.0, below category leaders sitting at 4.7. So the customer experience isn’t beating anyone on perceived quality.

But on the one metric we can see clean, the picture holds. Smaller brand. More absolute growth. Built around the way people now search.

If the catalogue says species and the customer says condition, the catalogue is the problem.

Stay human,

Sean