by Sean

by SeanIf you look at the headline number, UK plumbing is doing nothing. Up 0.01% over six months across 155 brands. Statistically, that’s a heartbeat with no pulse. Senior marketers see “+0.01%” and quietly drop the category off the next QBR slide.

6-month data refresh. Mid-cycle update of Salience Index Trade Plumbing data, not the full report. Request the latest refresh data.

Look closer. Screwfix, the canonical trade generalist, shed 444,325 organic visits between October 2025 and April 2026. That’s not a rounding error. That’s nearly half a million sessions of buyer demand that walked off the screen. Toolstation lost another 59,056. Two of the three biggest names in the sector quietly leaked over half a million visits in six months, and the sector still came out “flat.”

Where did the demand go? Not nowhere. It went somewhere specific. And the most useful example of where, the brand the data points at hardest, is a 28,000-review bathroom specialist called Big Bathroom Shop.

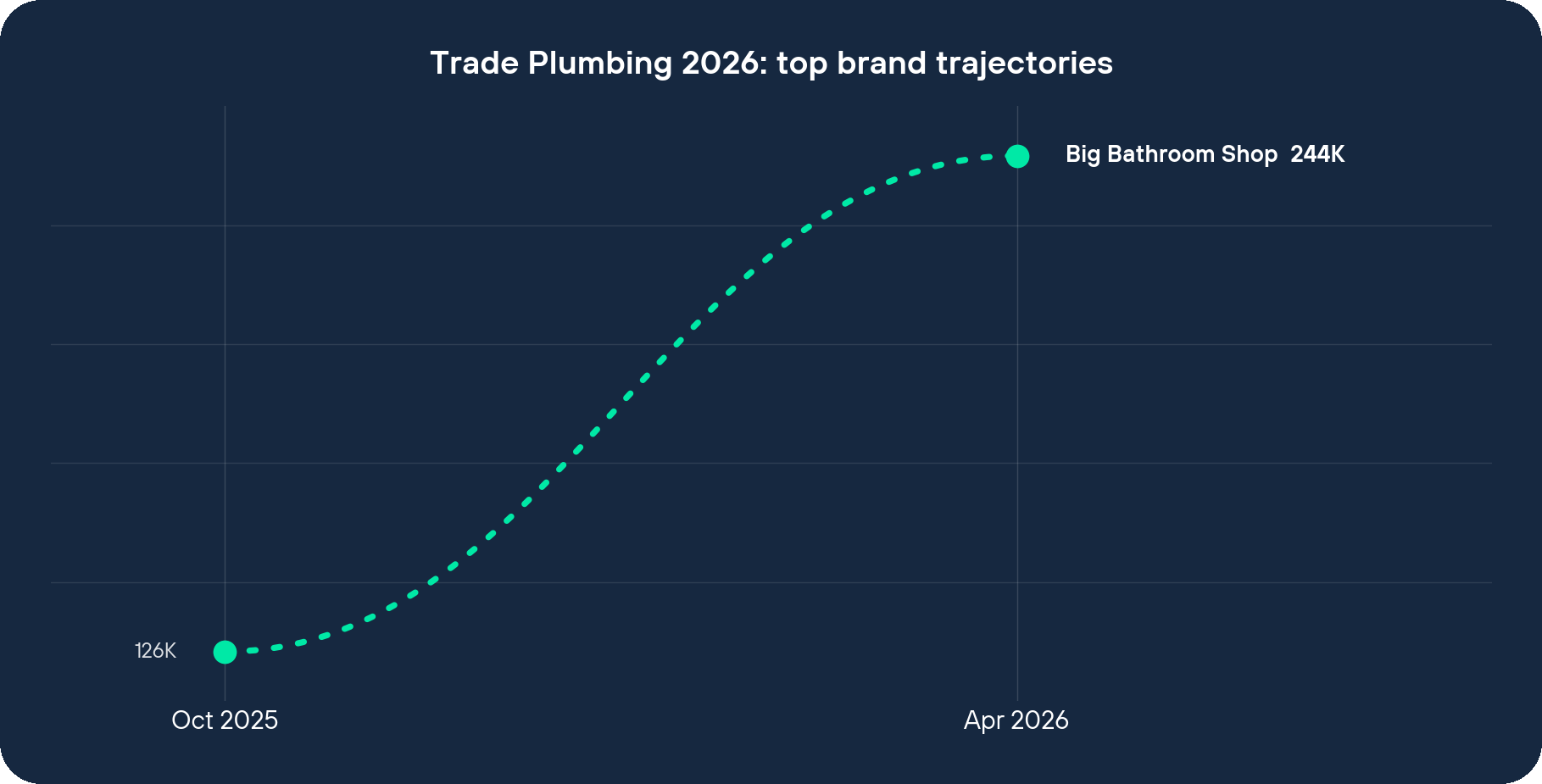

The numbers are ugly. Big Bathroom Shop went from 125,901 organic visits in October 2025 to 243,686 in April 2026. That’s +117,785 in absolute terms. +93.55% in relative terms. Nearly doubled, in six months, in a sector growing at one one-hundredth of a percent.

It is the largest absolute specialist gain in the entire 155-brand dataset. Rank 5 by absolute change. The four brands ahead of it are generalist giants moving their gigantic baselines. Big Bathroom Shop is the first name on the list that isn’t a national household.

Now run the comparison. Screwfix moved -5.63%. Big Bathroom Shop moved +93.55%. That’s a 99.18 percentage-point gap inside the same category, in the same six months, against the same UK buyers.

Then look at what surrounds it. Stelrad +35,579. The Radiator Warehouse +29,693. Radiator Outlet +26,345. City Plumbing +25,043. Plumbworld +20,381. Haldane-Fisher +18,798. Easy Bathrooms +18,605. Eight specialists, stacked, absorbing roughly 511,000 visits between them. Big Bathroom Shop alone accounted for about 23% of that absorption.

The headline “+0.01% market growth” was hiding a redistribution event. Demand didn’t leave the category. It moved from one column of the table to another.

Here’s the bet. Big Bathroom Shop has decided not to be a hardware brand.

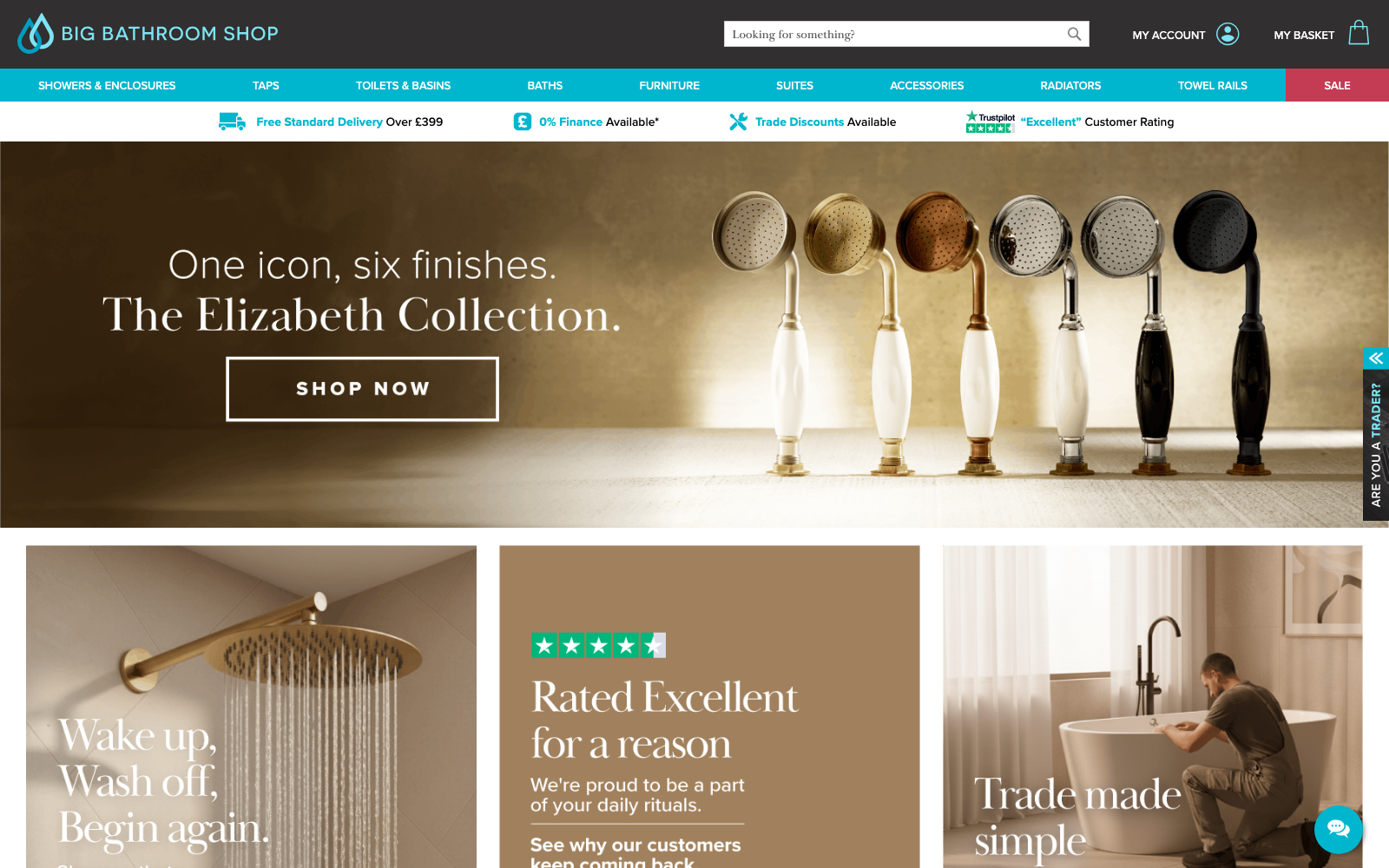

Look at the homepage. Suites. Baths. Showers. Taps. Furniture. Accessories. That’s it. No tools. No fixings. No paint. No extension leads sitting one row above a shower mixer. Zero category adjacency to anything that isn’t a bathroom.

That sounds obvious. It isn’t. The default move for an e-commerce brand at £125k-monthly traffic is to add categories, because more categories means more keywords means more sessions. Screwfix is the trophy version of that strategy: forty categories, hundreds of subcategories, ranking authority spread paper-thin across all of them.

Big Bathroom Shop has done the opposite. They’ve concentrated. Every page, every review, every blog post, every internal link, every backlink points at one product universe. The cost is real. They cannot serve a tradesperson buying a 22mm push-fit fitting and a tub of jointing compound on the same basket. The protection is bigger. When Google decides to reward category authority over horizontal breadth, which is what these numbers say is happening, a single-vertical site is structurally positioned to receive that reward.

Now walk the site.

You land on the homepage and the navigation is six categories wide. Each one expands into bathroom-only sub-filters. Shower type. Tap finish. Bath size. Suite style. You can filter a shower by “thermostatic” because that’s a normal word in a bathroom buyer’s vocabulary, and the site knows that.

Scroll down. Trust signals stacked, in order: 28,000+ Trustpilot reviews. 0% finance over £99. Trade discount tier. Free delivery over £399. 30-day money-back guarantee. Every one of those is calibrated to a £1k+ considered purchase. None of them make sense on a £4.99 blanking-cap journey.

Then the inspiration hub. “Big Bathroom Inspiration.” Lookbook galleries by style. Expert advice articles on tile choice, on lighting, on how to plan a small ensuite. This is top-of-funnel content with a budget behind it. A generalist treating bathrooms as one of forty product trees will not fund that. The maths doesn’t work for them. It does for a brand that is only ever in the bathroom SERP.

Now imagine you’re spec’ing a new ensuite. You type “thermostatic shower mixer small ensuite” into Google. The result that converts is the one stacked with bathroom-specific reviews, fitted into a planning journey, financed for a £1k purchase, and surrounded by shower-only filtering. Not the one sitting one row above a paint sprayer.

Now flip that on its head. The Screwfix product page for that same shower mixer is fighting for ranking authority with its own listings for extension leads, cement mixers, and timber screws. The model is brilliant for transactional trips. It is terrible for consideration-length queries. Sure, that’s partly a Google ranking thing. But a big part of that is incentive geometry. Screwfix earns its margin from frequency and basket size on tradesperson trips. Bathroom planning is a different job, and the horizontal model cannot fund a 28,000-review Trustpilot footprint inside one vertical. It cannot fund “Big Bathroom Inspiration.” It cannot ring-fence design content the way a specialist can, because every internal investment is split across forty categories.

The result, in the data, is a 99-point swing. One bathroom-only shop took more than a quarter of the visits that left Screwfix’s six-month window. That isn’t an SEO trick. That’s a structural reward for category concentration.

I’ve put myself on a tangent here, but stay with me. The thing that makes this uncomfortable for senior marketers is not the Big Bathroom Shop number. It’s what the number says about everyone else in the category.

The plumbing sector ran on a sensible assumption for fifteen years. Big horizontal generalists win because they capture every kind of trip. That assumption is still true for transactional trips. It is no longer true for considered ones. UK buyers do not type “where do I buy a shower valve” and “which shower valve should I buy” into the same SERP intent any more, and Google does not rank the same way against those two queries.

Anyway. Back to the point. If you are running marketing for a brand inside this category, you have a portfolio decision sitting on your desk that nobody is calling a portfolio decision. Every campaign that tries to win every kind of buyer is currently sub-funding the campaigns that could win one kind of buyer properly.

What becomes first-class, if this reading is right: vertical depth, review density per category, finance and design support, inspiration content that costs real money to fund. What becomes background: ranking against generalists on transactional head terms, because that fight is mostly lost on consideration-length queries.

The very fact that this looks obvious in retrospect is the organisational problem. Nobody gets fired for adding a category. People get fired for cutting one. “Why did we narrow?” is a meeting question that exposes a marketing director to blame. “Why did we widen?” never is. That asymmetry is why Screwfix’s structure persists, and why the specialist body of this market is eating the head.

One caveat, because the data window is six months, not five years. Some of Screwfix’s loss could be re-indexation, search-feature shift, or seasonality I cannot isolate from this period. Big Bathroom Shop’s gain could include a re-platform tailwind I have not seen the inside of. Both things might be partially true. But you do not get +117,785 visits and +93.55% growth from a re-index. You get that from a structural alignment with how the SERP is currently rewarding category depth.

Plumbing isn’t a flat market. It’s a redistributing one, and the brands set up to receive that demand are the brands that only ever sell one thing.