by Sean

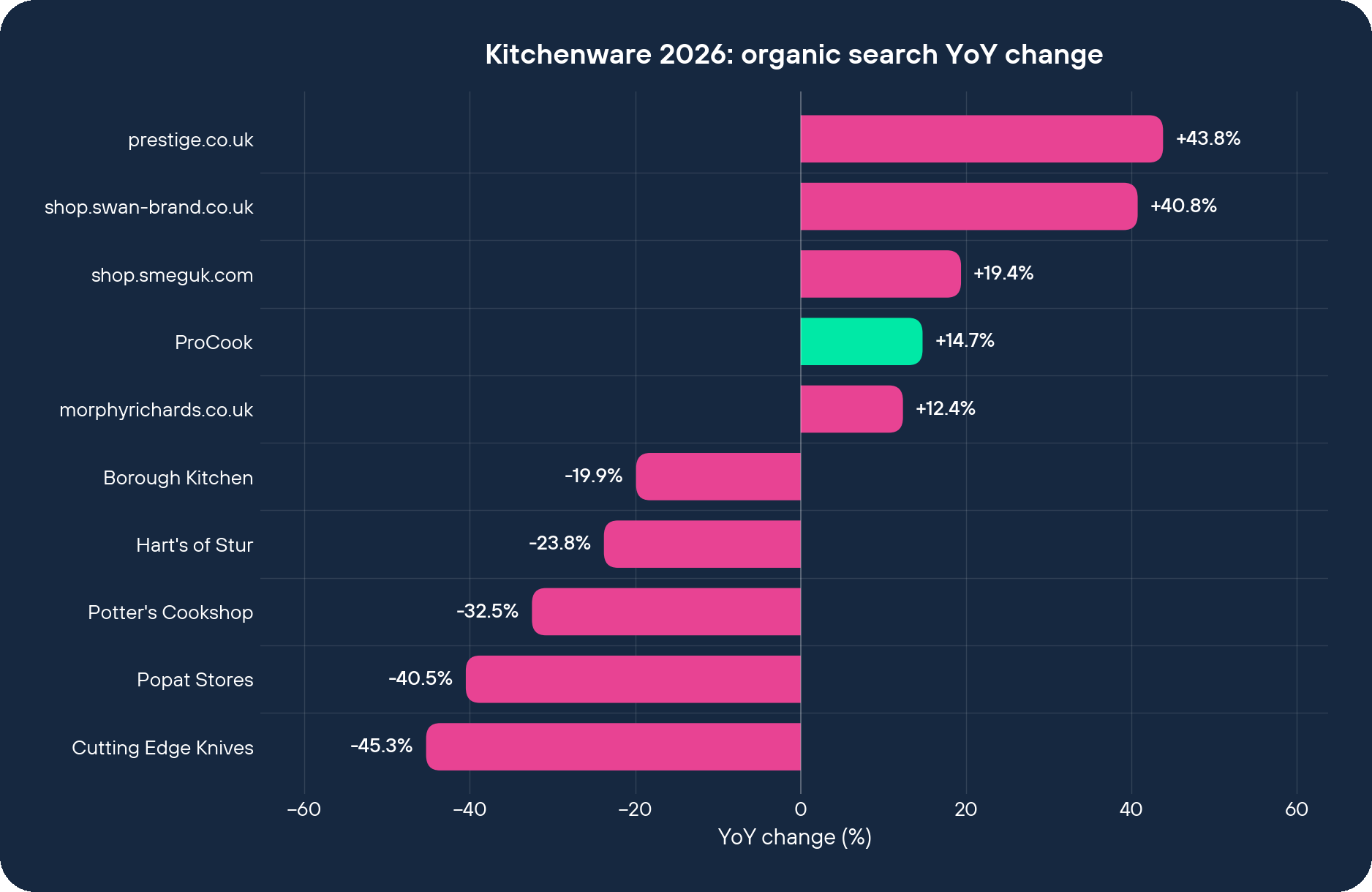

by SeanThe multi-brand kitchenware retailer is being dismantled in the SERP, and nobody at the multi-brand kitchenware retailer seems to have noticed. Hart’s of Stur lost 23.79% of organic visibility this period. Borough Kitchen lost 19.90%. Potter’s Cookshop lost 32.49%. Popat Stores lost 40.49%. Cutting Edge Knives lost 45.29%. None of them got worse at retail. None of them merchandised badly. They simply kept running the model that used to work, which was: “stock everyone’s product, become the trusted destination for cookware, get rewarded for breadth.” That model is over. Google now rewards the brand that owns the range, not the shop that aggregates it. ProCook is a useful example, because it is the single biggest gainer in the entire kitchenware dataset, and the reason it’s winning has almost nothing to do with marketing and almost everything to do with the SERP forgetting how to value the middleman.

6-month data refresh. Mid-cycle update of Salience Index Kitchenware data, not the full report. Request the latest refresh data.

Start with the number that does the most work. ProCook is now sitting at 394,264 monthly organic visits, up 14.74% in six months. To put that into context, that is bigger than Le Creuset (147,729 visits) and SMEG (119,706 visits) combined, and those are both heritage cookware brands whose Google footprint people assume is unassailable. ProCook absorbed 50,647 incremental visits in a single six-month window. Nobody else in the dataset added that many.

Now look at who lost. Hart’s of Stur, Borough Kitchen, Potter’s Cookshop, Popat Stores, Cutting Edge Knives. Multi-brand kitchenware retailers, all of them, all in the negative 19% to negative 45% range. No discernible operational difference between them. Same model, same fate.

Now look at who else gained. shop.smeguk.com +19.39%. shop.swan-brand.co.uk +40.75%. prestige.co.uk +43.82%. morphyrichards.co.uk +12.37%. karaca.co.uk +28.51%. Every one of them is a brand selling its own product directly. None of them is a multi-brand retailer.

A note on the headline. The kitchenware sector is reported at -11.90% YoY. That figure is almost entirely a SharkNinja domain migration: sharkninja.co.uk lost 489,786 visits in isolation. Strip that out and the SERP is roughly flat. The story isn’t decline. The story is who the demand redistributed to.

Look. ProCook’s bet is the single boring decision most kitchenware retailers refuse to make. They don’t sell other people’s brands. They are the brand. Cookware, knives, storage, electricals, tableware, baking, cast iron, accessories, all designed and sold under one name. That is the bet.

It costs them. They can’t put a Le Creuset signature pan in a category page to win the “Le Creuset” search. They can’t trade on KitchenAid’s century of brand equity. They can’t do the Hart’s-of-Stur trick of being “the trusted shop that stocks all the names you trust.” Vertical integration forces you to be the name yourself, which means you eat the cost of designing every product, the cost of being wrong about a product when you’re wrong, and the cost of building your own trust from scratch.

What it protects is the part nobody at the multi-brand retailer was watching. It protects their identity in the SERP. Because when Google ranks a “cast iron casserole” query, it increasingly wants the brand that makes the casserole, not the shop that resells the casserole. ProCook IS the casserole brand. Hart’s is the shop window. Same product on the shelf. Different rank.

Walk into procook.co.uk and you see the same nav a multi-brand retailer would build. Cookware. Kitchen Knives. Storage. Tableware. Electricals. Baking. Cast Iron. Accessories. That breadth used to be the multi-brand retailer’s only structural advantage. ProCook has it as a single entity Google can index.

Below the nav, three things are doing real SEO work, and not in a way most brands realise.

First, recipe content on the homepage. There’s a Greek-style spinach and feta filo pie sitting one scroll below the fold. That recipe isn’t decoration. It’s a content asset that lets ProCook rank for “spinach filo pie recipe” the way Hart’s of Stur cannot, because Hart’s is a shop and shops don’t write recipes. ProCook is a brand and brands publish content under their own entity.

I’ve put myself on a tangent, but stay with me. Most brands that publish recipes do it as “content marketing,” which means the page lives on a /blog subfolder, gets low internal-link weight, and ranks for nothing. ProCook has the recipe on the homepage, which means it inherits the homepage’s authority and competes for a real query. The reason I’m telling you this is that the same brand can publish the same recipe and get two completely different SERP outcomes depending on where the page sits. Anyway. Back to the point.

Second, a “Why buy from ProCook” rationale block, plus visible B Corp certification. The B Corp badge is doing two jobs: signalling trust to a buyer who increasingly cares, and giving Google an entity-graph signal that ProCook is a real organisation, not a reseller listing.

Third, 3-for-£20 and 3-for-£10 utensil bundles. ProCook owns those bundles end-to-end. Hart’s of Stur cannot bundle Le Creuset with Joseph Joseph at a fixed price because they don’t control either brand’s wholesale terms. The bundle SERP is now a ProCook SERP.

Conversion stack: Klarna pay-in-3, free delivery over £60, Trustpilot 4.8 out of 5 “Excellent,” in-store advice. Every box the multi-brand retailer ticks, ProCook ticks too, but at brand-equity prices, because the margin is theirs.

Now Hart’s of Stur, same period. Walk into hartsofstur.com and the homepage is, in order: Riedel Wine Tasting Evening, Seasalt clothing, Judge Cast Iron Casseroles, Villeroy & Boch Pura tableware. The categories include Clothing and Living. Their nav now reads “Country Department Store.” That is not a kitchenware brand. That is a Dorset shop hedging because they can sense the kitchenware retail position weakening. The problem is that Google does not index Hart’s as a department store. It indexes them as a kitchenware reseller competing with Le Creuset’s own .co.uk and ProCook’s own .co.uk for the same cookware queries. So the Seasalt section steals attention from the cookware section, the cookware section loses to the brands that made the cookware, and the model collapses sideways.

If this is right, a lot of teams need to change what they are measuring. The multi-brand kitchenware retailer’s biggest asset, range, is now their biggest liability. Stocking Le Creuset doesn’t make you findable on a Le Creuset query. It makes you a redirect to Le Creuset. Stocking KitchenAid doesn’t make you the destination for stand mixers. It makes you the place Google sends you on the way to KitchenAid.

The job has changed. It’s not “be the trusted retailer for great kitchen brands.” It’s “become an entity Google recognises as the source of something.” That requires either owning a product line end-to-end (ProCook), or specialising deep enough to be the category authority (souschef.co.uk +13.49%, bakerybits.co.uk +34.57%, cooksmill.co.uk +37.77%, all up).

Now imagine the buying meeting at a multi-brand kitchenware retailer where someone says, “we should drop Le Creuset and start manufacturing our own cast iron.” Everyone in the room laughs, because the suggestion sounds operationally insane. Now flip that on its head. The very fact that proposing it sounds insane is the proof that the norm is protecting itself. The model that’s quietly losing 23% a period is the safer-feeling option than the model that fixes the problem.

Here is the uncomfortable bit. Nobody at Hart’s of Stur is going to be fired for losing 23.79% of visibility when the headline market figure shows the sector down 11.90%. The market average becomes cover for a structural failure. “We’re outperforming the market” sounds fine in a board meeting. It also happens to be the sound of demand quietly redistributing to the brands the retailer used to broker.

A few honest caveats. This is a six-month organic visibility window. It does not capture paid media, in-store revenue, or repeat-purchase economics, all of which Hart’s of Stur, Borough Kitchen and the others rely on. ProCook has 60-plus retail stores of its own and a 20-year head start on the bet, so this isn’t a cheap pivot anyone can replicate next quarter. The redistribution could slow. But the pattern across every multi-brand loser and every brand-direct gainer is too clean to be noise.

If your only structural advantage is range you don’t own, you’re not a retailer. You’re a redirect.