by Sean

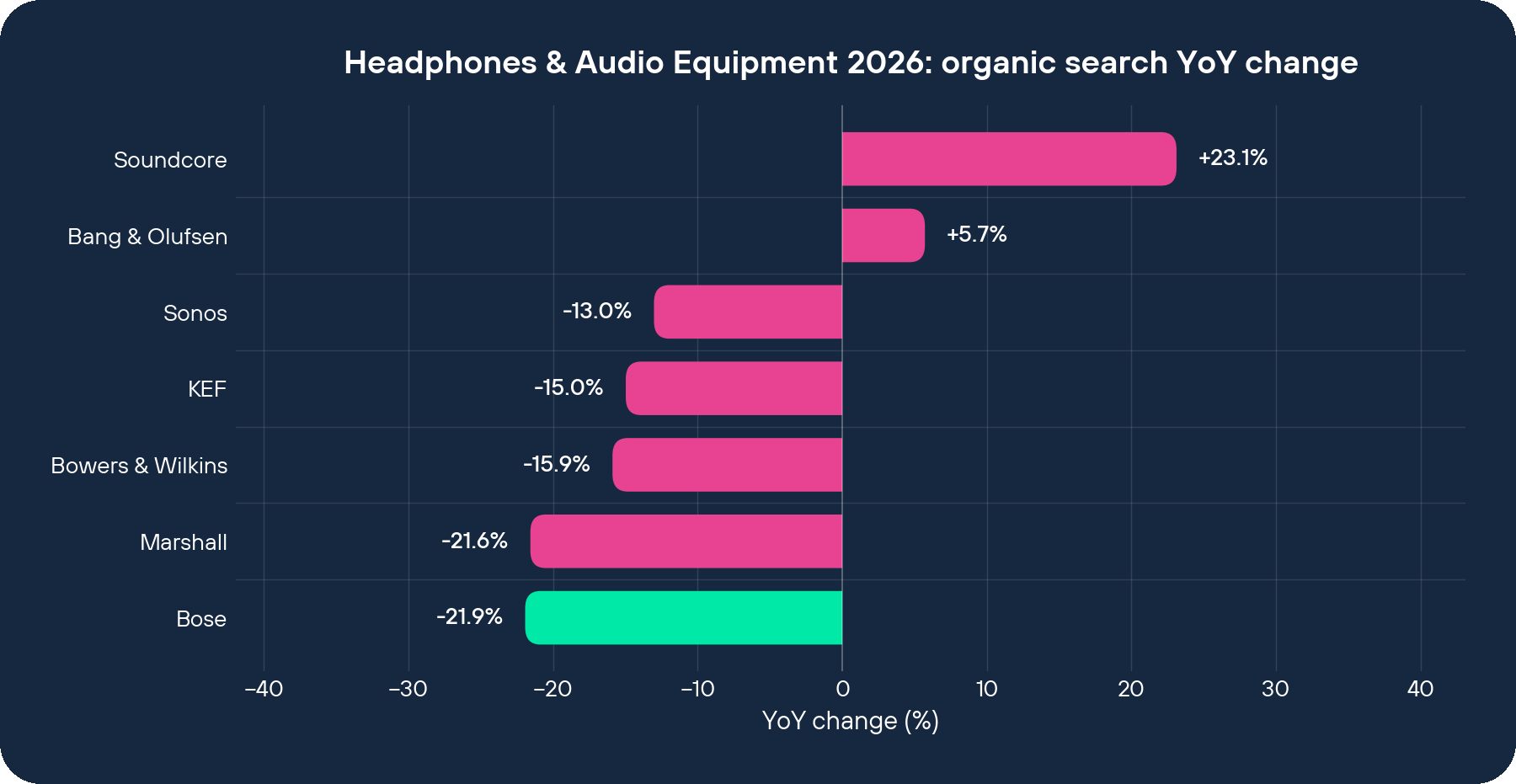

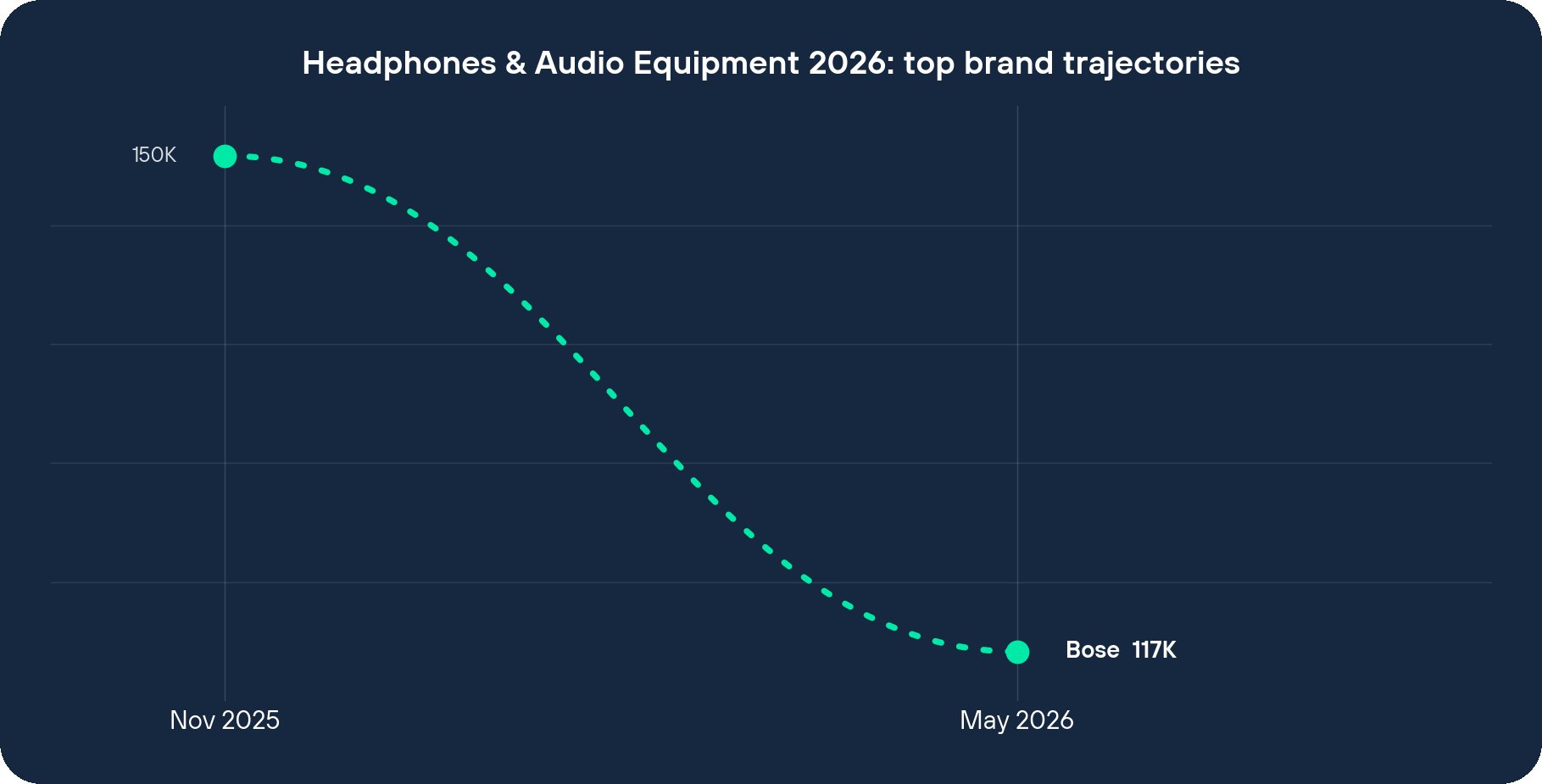

by SeanBetween November 2025 and May 2026, Bose’s UK organic visibility fell from 150,458 to 117,463 monthly visits to bose.co.uk. That is a loss of 32,995 visits, or -21.93% in six months, against a UK Headphones & Audio Equipment market that declined -6.61% across 152 brands over the same period. Bose now ranks 9th in our index, and its absolute six-month loss is larger than any other brand in the dataset apart from gear4music.com (-111,811). Among mid-premium specialists, Bose stands alone: Sonos lost 14,488 visits (-13.02%), Marshall lost 9,918 (-21.57%), KEF lost 3,571 (-14.97%) and Bowers & Wilkins lost 3,094 (-15.89%). Bose’s absolute loss is 2.3× larger than Sonos and 3.3× larger than Marshall.

6-month data refresh. Mid-cycle update of Salience Index Headphones & Audio Equipment data, not the full report. Request the latest refresh data.

The cohort matters. Every mid-premium specialist in the index is down. Bose alone accounts for just over half of the cohort’s combined six-month loss. So the brand that built the consumer category for noise-cancelling headphones, smart soundbars and lifestyle home speakers in the £400-£900 range is also leading the decline of that tier.

The growing brands sit on either side of Bose’s price band. Bang & Olufsen, which sells the Beoplay HX at £499 and the Beo Grace earbuds at £1,099, grew +5.72% (+1,798 visits) in the same six months and now ranks 22nd, which is +12.33 percentage points against the market. Soundcore, which sells the Space One Pro at £199, grew +23.12% (+7,332 visits) and now ranks 18th. Both flanks of Bose’s product range posted positive numbers against a falling market. The middle did not.

Bose’s product range collides with B&O above and Soundcore below

The QC Ultra Headphones at £449 are the clearest illustration. They are priced within £50 of B&O’s Beoplay HX (£499) and within £250 of Soundcore’s Space One Pro (£199). A buyer searching for noise-cancelling headphones in this price band has three brands they recognise. Two of them now offer a clearer story to a review-driven search ecosystem: B&O wins on material and craft (anodised aluminium, wool finishes, a lifetime-ownership narrative); Soundcore wins on price-to-feature comparison content that consistently performs on YouTube and on review aggregators. Bose’s own product detail pages lead with feature counts, active noise-cancelling modes, transparency modes, codec support, battery life.

The Smart Soundbar 900 at £899 sits in the same kind of squeeze. Sonos and Samsung occupy the surrounding price points with stronger third-party review presence, and B&O’s home-theatre range has taken the design-led editorial attention that used to belong to Bose a decade ago. The Home Speaker 500 at £549 faces a comparable problem: Sonos at the adjacent price point with stronger review-aggregator visibility, B&O at the tier above with editorial weight on materials and design.

bose.co.uk is built for commercial-intent terms it no longer wins

The site’s category pages are product-led. The headphones page is a product grid with filters for headphone type and noise-cancelling level, sorted by price. The on-page content sells the products themselves but does not function as standalone reference content for category-level search intent.

bose.co.uk leans on broad commercial-intent queries, best noise cancelling headphones, wireless speakers, best soundbar, where the site is one of fifteen retailers and review publishers competing on the first page. These are also exactly the queries where third-party publisher content (What Hi-Fi?, RTINGS, The Verge) is structurally favoured by Google, and where AI Overview citations are increasingly going to review aggregators rather than to manufacturers.

Bose’s organic visibility therefore concentrates on brand-driven searches (bose qc ultra review, bose soundbar 900) and on a small share of generic queries. When the brand-search volume softens, which it has done since the post-pandemic peak in personal audio, and which the -6.61% market decline reflects, bose.co.uk has no editorial topical authority on category-level content to backfill the loss. There is no equivalent on the site to the review-comparison content Soundcore publishes, to the long-form buyer guides that drive top-of-funnel category discovery, or to the brand-heritage editorial that B&O publishes at the tier above.

Bang & Olufsen built the inverse footprint

B&O’s homepage opens with the launch of Beo Grace at £1,099, the 100-year heritage line (“A Century of Craftsmanship. A Future Icon”), and a customisation tool offering more than 500,000 colour, material and finish combinations across the catalogue. The product ladder runs from £169 (Beosound Explore) to £3,499 (Beosound Premiere), with editorial weight concentrated in the upper half of the range. The Beoplay H100 sits at £1,499. The Beosound A9 is £2,749. The Beosound A5 is £1,299.

The Beo Grace product detail page runs through nine product images and leads with material and craft language; the technical specification (advanced ANC earbuds, hand-polished finish) appears below the editorial setup, not above it. The House of Bang & Olufsen membership page sells exclusive launches, events and personalised content. The site competes on brand-led discovery at a price tier where the buyer either already knows B&O or sits outside the target customer profile entirely.

B&O grew +5.72% (+1,798 visits) in a market that fell -6.61%. The absolute scale is small, B&O has 33,225 monthly visits against Bose’s 117,463, so this is not a story about B&O overtaking anyone in raw traffic. The point is that B&O sits in the price tier above Bose, and the price tier above Bose is the one still growing.

What else might be driving Bose’s decline

Several things plausibly contribute that are not visible in this dataset, and an honest read has to name them.

First, the November-to-May comparison is a hard seasonal one. November includes pre-Christmas brand-search peaks for consumer audio. May is structurally quieter for purchase intent in the category. Some portion of the -21.93% reflects a strong base period being compared against a weak one. A May 2025 to May 2026 comparison would give a cleaner read on underlying trend.

Second, Bose’s retail distribution has shifted. The brand has been pushing more volume through its own DTC channel over the last two years, which affects the retailer affiliate ecosystem, the deal-aggregator content, and the third-party comparison pages that drive ancillary organic traffic to bose.co.uk. Some of the visibility decline may be offset by gains on retailer pages outside our measurement scope.

Third, the headphones category as a whole has softened since the post-pandemic personal-audio peak. The market is down -6.61% across our 152-brand index, and Bose’s overweight position in headphones (versus, for example, LG’s overweight in soundbars and televisions, or Sony’s broader audio-visual portfolio) exposes them more directly to that category-level softness.

Fourth, paid media sits outside this dataset. If Bose has shifted media spend from brand-building campaigns (which drive branded organic search downstream) into performance retargeting (which does not), the organic visibility decline will overstate the underlying commercial decline. We cannot see that movement from here.

None of this changes the headline observation. Bose’s six-month organic visibility decline is 2.3× larger than the next biggest mid-premium loser and is happening while the price tiers immediately above and below Bose are growing. In a 152-brand dataset, no other brand illustrates the mid-premium hollowing-out more directly: a household name with strong distribution and high category awareness, priced into a band where cultural permission to spend is thinning, on a website built for brand-led search behaviour that is increasingly being displaced by review-led publisher content and by AI-cited comparison pages from brands sitting above and below.

For marketing and ecommerce leads watching the same pattern in their own category, two practical areas of work follow. Ecommerce category and product page SEO rebuilds PLPs and PDPs so they function as reference content for category-level search rather than as product grids alone. Content strategy for AI Overview citations builds the editorial topical authority that now determines who gets cited in AI Overviews and that backfills softening brand-search demand. If your category looks like Bose’s, recognised name, strong distribution, organic visibility quietly falling against the tiers above and below, those are the two places to start.

Further reading

- 2025 Consumer Electronics Market Report, Consumer electronics is the closest adjacent sector and gives readers context on how the wider category is performing beyond audio specifically.

- Mid-premium squeeze in UK car dealerships, The same mid-premium hollowing-out pattern appears in another big-ticket UK category, so this gives a useful cross-sector comparison.

- 2025 Fitness Equipment Market Report, Another discretionary consumer category facing similar price-tier pressure, useful for benchmarking against parallel markets.

- All Salience Index sector reports, A single hub to browse every sector benchmark if you want to compare Headphones & Audio against other UK markets.