by Sean

by Sean

Start with the number everyone will quote

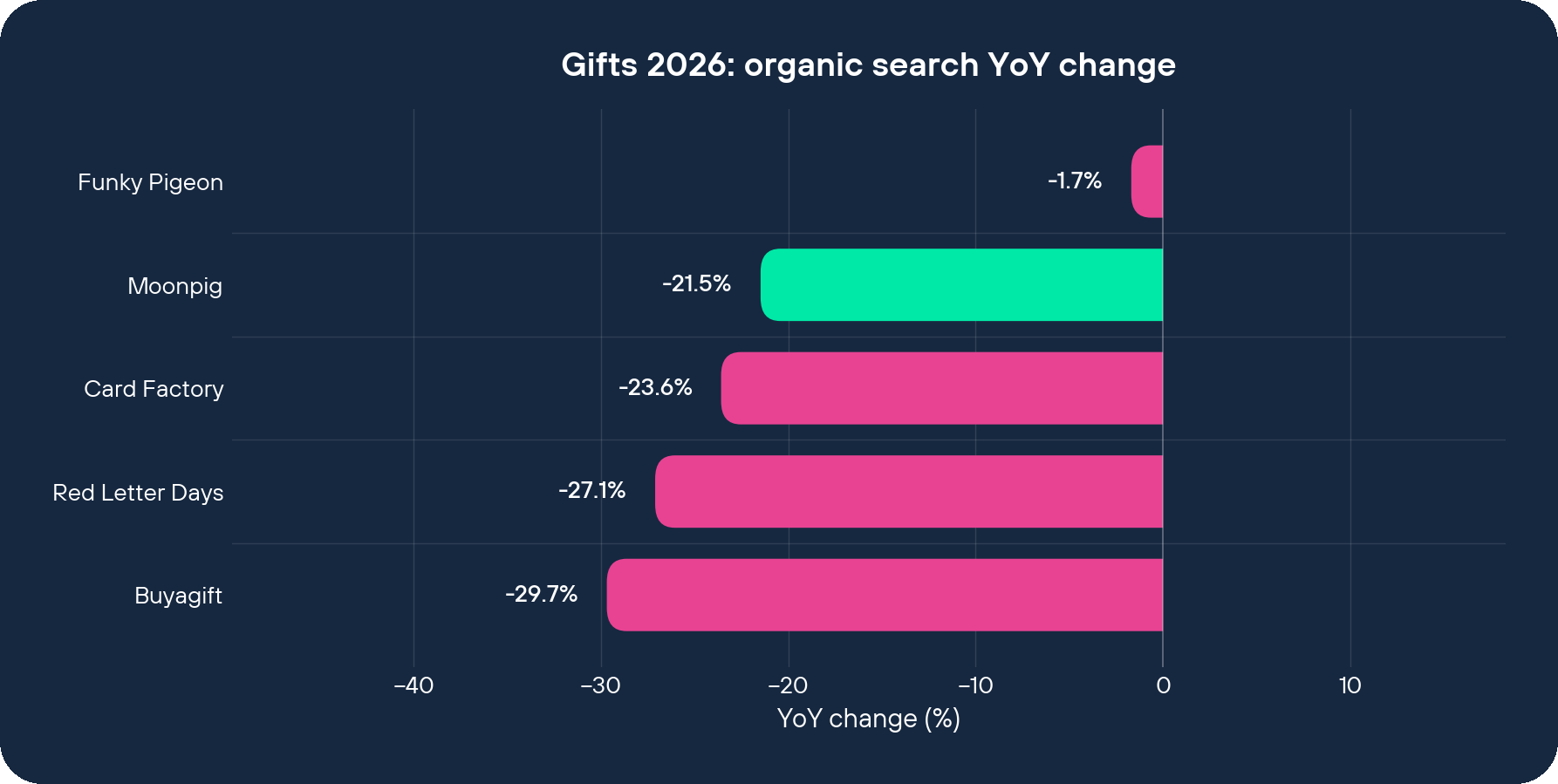

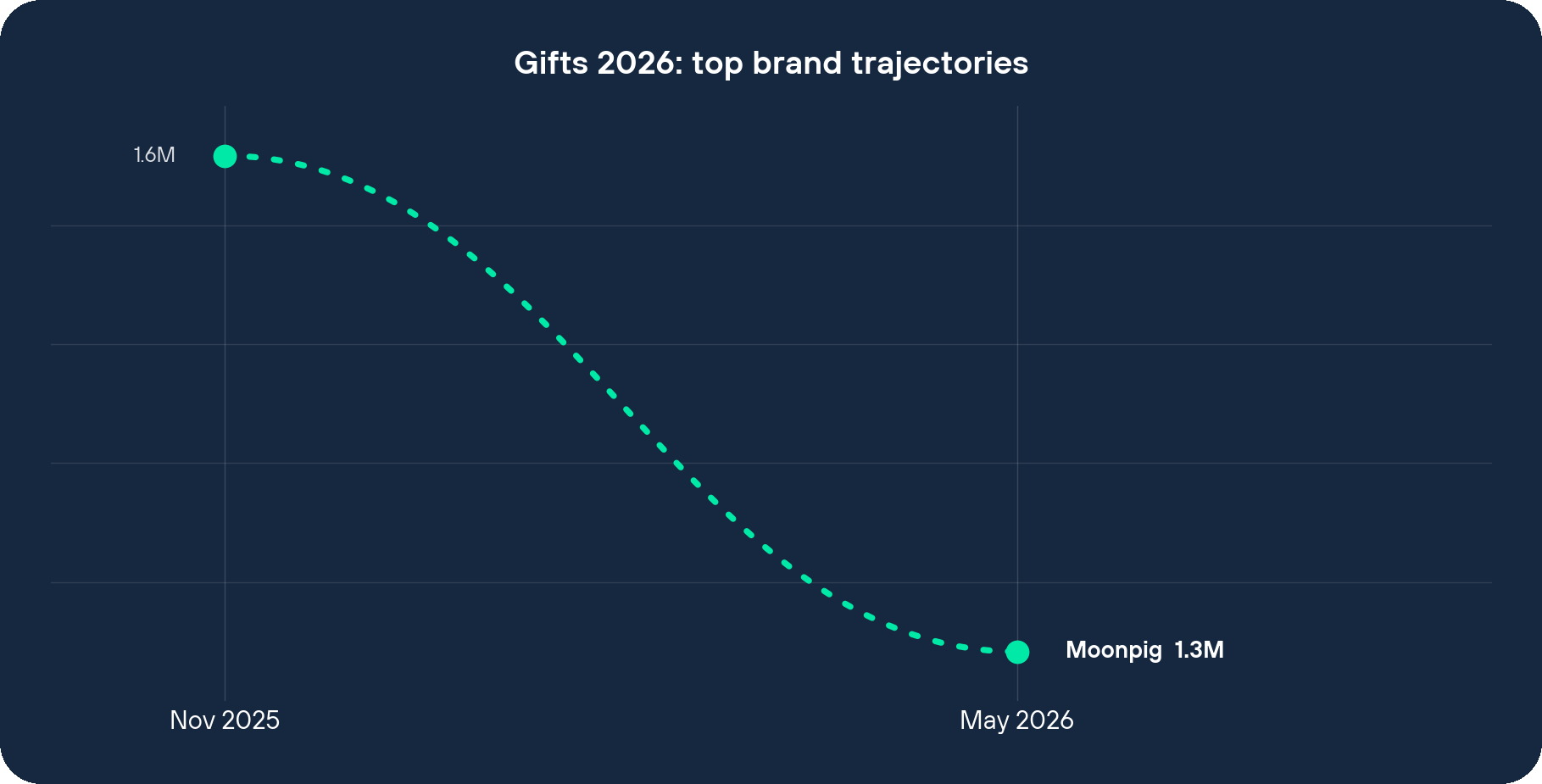

Moonpig lost 348,973 in estimated organic visibility between November 2025 and May 2026, falling from 1,624,553 to 1,275,580. That is the largest absolute drop of any of the 154 brands in this dataset, and it is the figure that will get pulled into the headline. It is worth slowing down on before anyone builds a story around it. Click below to access the latest Gifts market report.

In percentage terms Moonpig fell 21.48%. The market fell 20.56%. Moonpig’s decline measured against the market was therefore -0.92%, under a single percentage point worse than the sector average. By rate, Moonpig is unremarkable. It declined at almost exactly the pace the whole category declined.

The reason the absolute figure is so large is that Moonpig started from 1,624,553, well ahead of the next brand, Card Factory, at 1,125,820. When an entire sector contracts by a fifth, the brand with the most visibility to begin with loses the most in raw numbers, close to arithmetically. So the “biggest drop in the sector” line is mostly a consequence of Moonpig being the biggest brand in the sector.

That does not make the decline meaningless. It tells you Moonpig fell exactly as fast as the average, and the question worth asking is why a brand this dominant could not do better than average when so much of its visibility is attached to a name almost everyone in the UK recognises.

A site built to win the search that AI Overviews now answer

Spend two minutes on moonpig.com and the answer starts to show. The homepage is organised around occasion tiles, Birthday, Anniversary, Thank You, and price-point shelves such as “£20 & under” and “gifts from £9.99”. The footer SEO copy targets “greetings cards for every occasion”, “birthday cards”, “anniversary cards” and “thank you cards”. Every one of those is a generic, undifferentiated category term, and not one of them contains the word Moonpig.

That body of copy was built to rank for the “what should I buy” layer of search, someone typing “birthday gift ideas” or “anniversary cards” with no brand in mind. For fifteen years that was the most valuable position to hold in gifting search, and Moonpig won a large share of it. It is also precisely the layer AI Overviews now resolve inside the results page. When Google answers “good thank you gift ideas” directly above the organic listings, the ranking position Moonpig holds for that term still exists, but far fewer people click through, because the answer is already on the page.

So a large part of Moonpig’s visibility was attached to exactly the queries that lost their clicks first, and the decline is consistent with that. I would caution against crediting all of it to AI Overviews, and I’ll come back to the other drivers at the end.

Knowing the name and searching the name are different things

Moonpig is one of the most recognised retail brands in the country. It is listed on the London Stock Exchange, it advertises heavily on television, and “I’ve Moonpigged you” is close to a verb. The reasonable assumption is that this protects it. The data says it did not: Moonpig lost more than any brand here, and Card Factory, another household name whose visibility comes from generic terms like “birthday cards” and “Christmas cards”, sits second on the list with a drop of 265,535 (-23.59%).

What protects organic visibility through a shift like this is people typing your name into the search box, because a search for “moonpig” has no AI Overview standing between the searcher and the site. Brand awareness and branded search volume are separate things. Plenty of people know Moonpig perfectly well and still arrive at it by searching “personalised birthday card”, and that is the traffic that thinned out. Recognition is worth a great deal commercially; it simply was not the part of Moonpig’s visibility that was exposed here, and the same thing plays out in why famous brands struggle in organic search.

Moonpig Group’s other businesses fell the same way

Moonpig is one brand inside a larger group. Moonpig Group plc owns Greetz in the Netherlands and, since 2022, the experience-gifting businesses Buyagift and Red Letter Days. Three of those brands appear in this dataset, and all three fell.

Buyagift lost 159,312 (-29.69%, rank 6). Red Letter Days lost 51,570 (-27.11%, rank 12). Add Moonpig’s 348,973 and the group lost 559,855 in estimated visibility across the period. Both experience businesses fell harder than the market, Buyagift at -9.13% against it, Red Letter Days at -6.55%, where Moonpig itself came in roughly in line at -0.92%.

That is consistent, because experience gifting leans even more heavily on discovery search than cards do. “Experience days for him”, “things to do as a gift” and “spa day vouchers” are the same browse-led, undifferentiated queries, and they are just as answerable inside an AI Overview. Across cards, flowers and experiences, the group’s traffic has been built on people searching for an occasion or a recipient and being shown a list of options, which is the precise behaviour AI Overviews now intercept. The decline is a group-wide exposure, not a quirk of one brand’s homepage.

Funky Pigeon held flat with the same business and a different shopfront

The clearest evidence sits with Moonpig’s nearest direct rival. Funky Pigeon, the long-established online card-and-gift retailer, fell just 1.69% over the same period (rank 8), which put it 18.86 percentage points ahead of the market. Same products, same print-and-post model, same sector falling by a fifth around it. The difference shows up the moment you open the menu. Funky Pigeon’s navigation is built around a “Who’s it For” section, For Her, For Him, For Kids, Mum, Dad, Wife, Husband, and a long licensed-brand list running through Bluey, Disney, Harry Potter, Peppa Pig, Pokemon and Me to You. Those are searches people make by recipient and by character, like “Bluey birthday card” or “Disney card for mum”, and they carry a buying intent an AI Overview does not satisfy, because the shopper still wants to browse the actual designs and personalise one. Funky Pigeon’s menu happens to sit closer to the kind of demand that survived the period.

I would not over-read this. Funky Pigeon is roughly a sixth of Moonpig’s size, and a smaller brand losing 4,721 is not the same test as one moving across 1.6 million. But the direction is clear, and the on-site evidence for why is sitting in the navigation of both sites for anyone to read, and getting that right is the work of ecommerce category and navigation SEO.

What it actually costs Moonpig

Two cautions before anyone over-reacts to the 348,973. First, the comparison runs from November to May. November is the run-up to Christmas, the single biggest card-buying period of the year; May is comparatively quiet. Some of the absolute fall is seasonal search behaviour that affects every brand in the table, which is part of why the against-the-market figures are the more honest read, they net most of that out, and on that measure Moonpig performed in line with the sector.

Second, organic discovery is only one of Moonpig’s acquisition channels, and the company has told the market for years that it is a smaller one. Moonpig has consistently reported that a high share of its orders come through its app and its reminders feature, from customers it already has. A loyal, repeat customer does not appear in an organic visibility table at all. The 348,973 is real, but it overstates the commercial damage, because much of Moonpig’s revenue never depended on ranking for “thank you gifts” in the first place.

Where it does bite is new-customer acquisition. The generic, occasion-led search that thinned out is how Moonpig reaches people who do not already have the app, the top of the funnel rather than the repeat orders. If AI Overviews keep absorbing those queries, Moonpig meets fewer first-time customers through search, and over several reporting periods that slowly narrows the flow of new people into the kind of repeat relationship its app and reminders are unusually good at holding onto.

If your brand is exposed to the same generic, occasion-led queries, the way to keep meeting first-time customers is to earn a place inside the answers themselves with content built for AI Overview citations. You can see where your own brand sits across the gifting sector by downloading the full Salience Index data.

Further reading

- Jellycat’s growth on searches rivals can’t rank for, The encouraging counterpart to Moonpig, showing a gifting brand that grew because its demand sits in branded searches AI Overviews cannot answer.

- Salience Index greetings cards report, Moonpig is first of all a greetings cards retailer, so the dedicated cards report gives the closest sub-sector benchmark for its visibility.

- Salience Index florist sector report, Flowers sit in the same gifting group as cards and experiences, and this report shows how the adjacent florist category moved over a comparable period.