by Sean

by SeanThe narrative running through this period is that Britain’s bargain and second-hand booksellers are losing ground in search, while branded destinations and publishers absorb the demand that used to land on them. World of Books is the clearest single illustration of that, and it’s worth profiling precisely because the easy explanations for its decline don’t survive contact with its own brand numbers. Click below to access the latest Booksellers market report.

The biggest single loss in the market

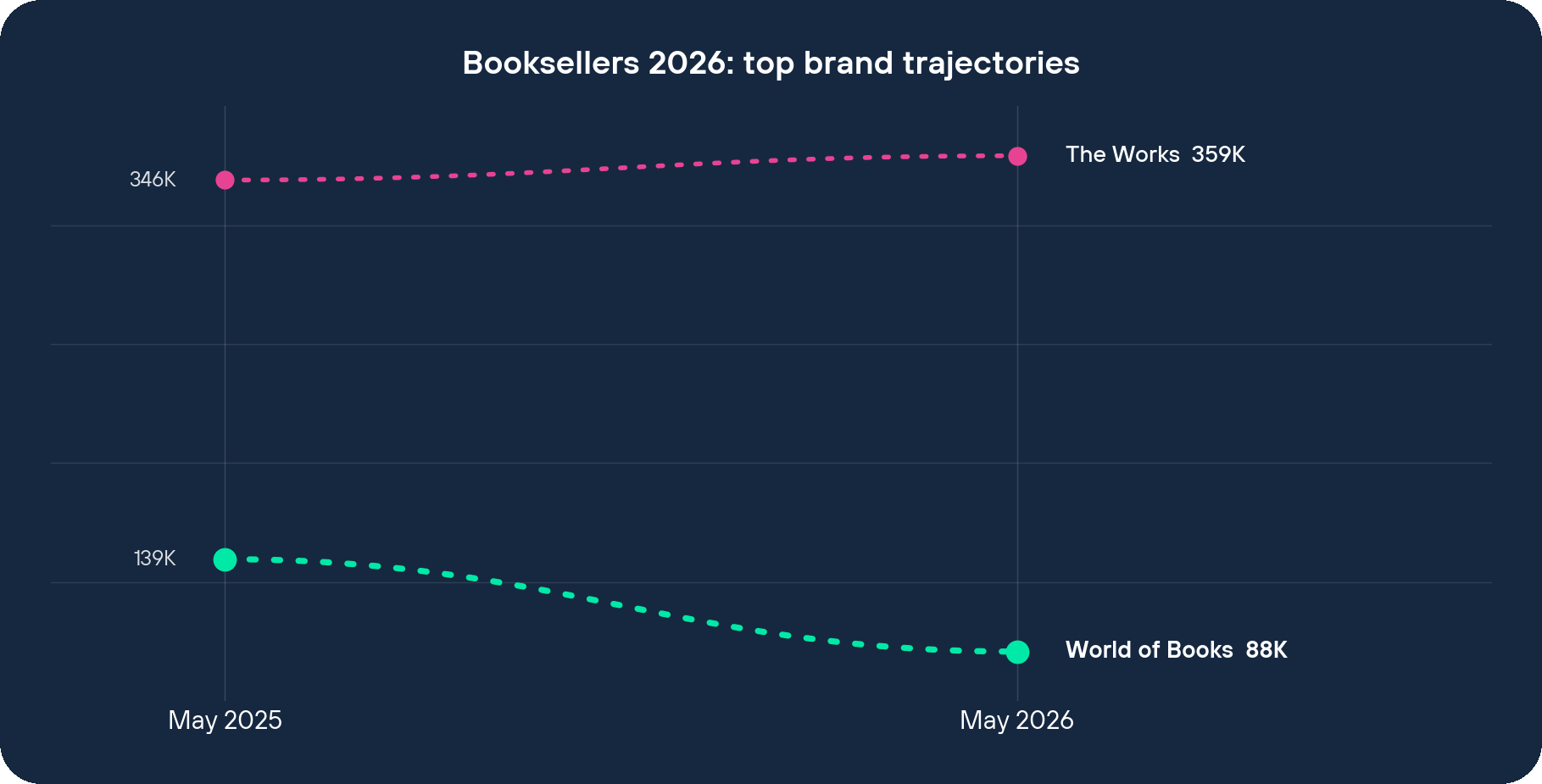

World of Books went from 138,653 monthly visits in May 2025 to 88,110 in May 2026, a loss of 50,543 visits and a fall of 36.45%. Against a market that contracted by 5.0% over the same twelve months, that is 31.45 points worse than the average bookseller. It is the largest absolute drop of any of the 275 brands in the dataset: bigger in raw visits than AbeBooks (-29,226), bigger than Books2Door (-20,486), and bigger than the decline at any other site in the sector.

This happened from a position of strength. World of Books is still the third most visible bookseller in the dataset, behind only Waterstones (536,242) and The Works (359,397). One of the three biggest organic destinations in UK bookselling lost more than a third of its visibility in a year.

The brand search and the reviews held up

The usual first explanation for a drop this size is that the brand lost relevance, fewer people searching for it, eroding trust, a reputation problem. None of that fits here.

World of Books carries 246,000 monthly brand searches, which places it seventh in the sector on Salience’s Brand Reach score, ahead of established names like Foyles, Blackwell’s and Folio Society. On reviews it sits second only to ThriftBooks across the entire market, with 519,774 reviews at an average of 4.6 stars. People are still searching for “World of Books” by name in large volume, and the ones who buy are rating the experience at 4.6 stars. Awareness and trust are clearly intact.

So the 36.45% fall happened while brand demand and customer satisfaction stayed strong. That rules out the easy answers and points the question somewhere more specific: what kind of search traffic was World of Books actually capturing, and what happened to it.

What the homepage is built to capture

Spend a minute on worldofbooks.com and the answer is visible in how the homepage is put together. The hero line is “OVER 100 MILLION BOOKS REHOMED”, which sells scale and sustainability rather than a specific reason to choose this shop over another. Below it, the page is organised around genre tiles, Fantasy, Romance, Thriller, Classic Fiction, with rows of recently-viewed titles and a free service that lets customers send in their old books for credit.

Every one of those choices is built to win the same kind of search: someone looking for a specific cheap title, or browsing a broad genre, with no particular loyalty to where they buy it. Queries like “used fantasy books”, “second-hand [title] cheap” and “sell my old books” are substitutable and price-led, where the cheapest acceptable result wins. That worked extremely well for years, and it built the visibility and the review count World of Books still has.

It is also exactly the kind of query that has become harder to win in the last year. Title-level and genre-level searches are the most substitutable demand in the whole sector, and the easiest for a price-comparison result, a marketplace listing, or an AI Overview to satisfy before anyone clicks through to a bookseller’s own site. World of Books built its visibility on the most exposed search demand there is, and that demand is the part of the market shrinking fastest.

The whole second-hand cohort moved together

If this were a World of Books problem, it would show up as World of Books underperforming its peers. It didn’t. The entire used and discount group fell together, and most of it fell hard against a market down only 5.0%.

AbeBooks, owned by Amazon, lost 25.77%. Books2Door fell 26.54%. Oxfam’s charity-run online shop dropped 23.26%. Further down the visibility table the declines get steeper: ThriftBooks down 68.50%, Wordery down 64.64%, Biblio down 84.87%. These are businesses with completely different owners, budgets and catalogues. The one thing they share is the same kind of site and the same kind of search demand, cheap, substitutable titles sold on price and availability. When a group this varied moves the same way at the same time, the cause is the model they have in common, not anything specific to one of them. World of Books is the most visible example of that model, which is why it posted the largest absolute loss. There’s more on World of Books and search behaviour in our deeper look at booksellers’ brands.

What The Works did instead

The Works grew, and looking at how shows what World of Books’ position lacks. It went from 346,118 visits to 359,397, up 3.84%, 8.84 points ahead of the market, and it did this as the second most visible site in the sector.

The Works’ homepage leads with “Affordable Screen-Free Fun for the Whole Family” and organises the site around licensed brands people search for by name: Bluey, Harry Potter, Disney, Marvel, Squishmallows, alongside its 500+ UK stores. That gives it branded and category demand that doesn’t depend on substitutable title queries. People search “Bluey book”, “Harry Potter gift” or “The Works near me”, and those searches are far harder for an aggregator or an AI Overview to intercept. The Brand Reach data backs this up: The Works carries 673,000 monthly brand searches, the highest in the sector and nearly three times World of Books’ 246,000.

It’s worth being clear about what this contrast does and doesn’t prove. The Works is a 500-store retailer with its own seasonal ranges, licensing deals and paid marketing, and its growth has more than one cause. But it grew without the enormous review count World of Books has, The Works doesn’t even appear in the sector’s top 20 by review volume. Review count and brand search were never going to protect World of Books from a fall in the specific kind of search its site depends on, and the contrast makes that plain.

The honest read on the numbers

Before crediting any single cause, it’s worth stating what this dataset can and can’t see. It measures organic search visibility to each brand’s own domain. It does not see paid search, and it does not see marketplace sales, and World of Books sells heavily through Amazon and eBay. A 36.45% fall in organic visibility to worldofbooks.com is not the same as a 36.45% fall in the company’s sales. Some of the lost discovery traffic may now be landing on those marketplace listings instead, where the same substitutable-title demand is even easier to satisfy.

There are other drivers worth naming honestly. The May 2025 to May 2026 window covers a period when AI Overviews expanded heavily across UK commercial and informational queries, which is the most plausible single reason substitutable-title searches are converting to fewer clicks on booksellers’ own sites, but this dataset shows the symptom rather than that specific cause, so it stays a hypothesis. World of Books may also have lapped an unusually strong May 2025, which the data here can’t confirm either way.

The point that does hold, because the whole cohort moved together, is the structural one. Across very different owners, budgets and catalogues, the second-hand and discount group built its visibility on the most substitutable search demand in the sector, and that demand is contracting faster than the market. For anyone running search in this category, the read on World of Books is straightforward: brand strength and review volume are real assets, and they did not defend visibility built on price-led, title-level queries. World of Books, as the most visible site sitting on exactly that kind of demand, registered the largest fall of anyone.

If you’re running search for a bookseller, or any retailer exposed to the same price-led demand, there are two practical responses. The first is content built for AI Overview citations, so your site earns the topic authority that keeps readers clicking through when an AI Overview tries to answer the query first. The second is category and product page optimisation, so the genre and title pages that capture browsing demand are strong enough to hold it. Salience works on both.

Further reading

- 2026 Toy Stores Industry Report, The Works competes on licensed toy and character brands, so the toy sector report shows the wider category demand that helped it grow while booksellers fell.

- 2025 Charities Industry Report, Oxfam’s charity-run shop is one of the second-hand sellers that fell here, and the charities report shows how that sector performs in search more broadly.

- every Salience Index sector report, Readers comparing how booksellers fared against other retail categories can browse the full set of sector reports from one place.