by Sean

by Sean

The number

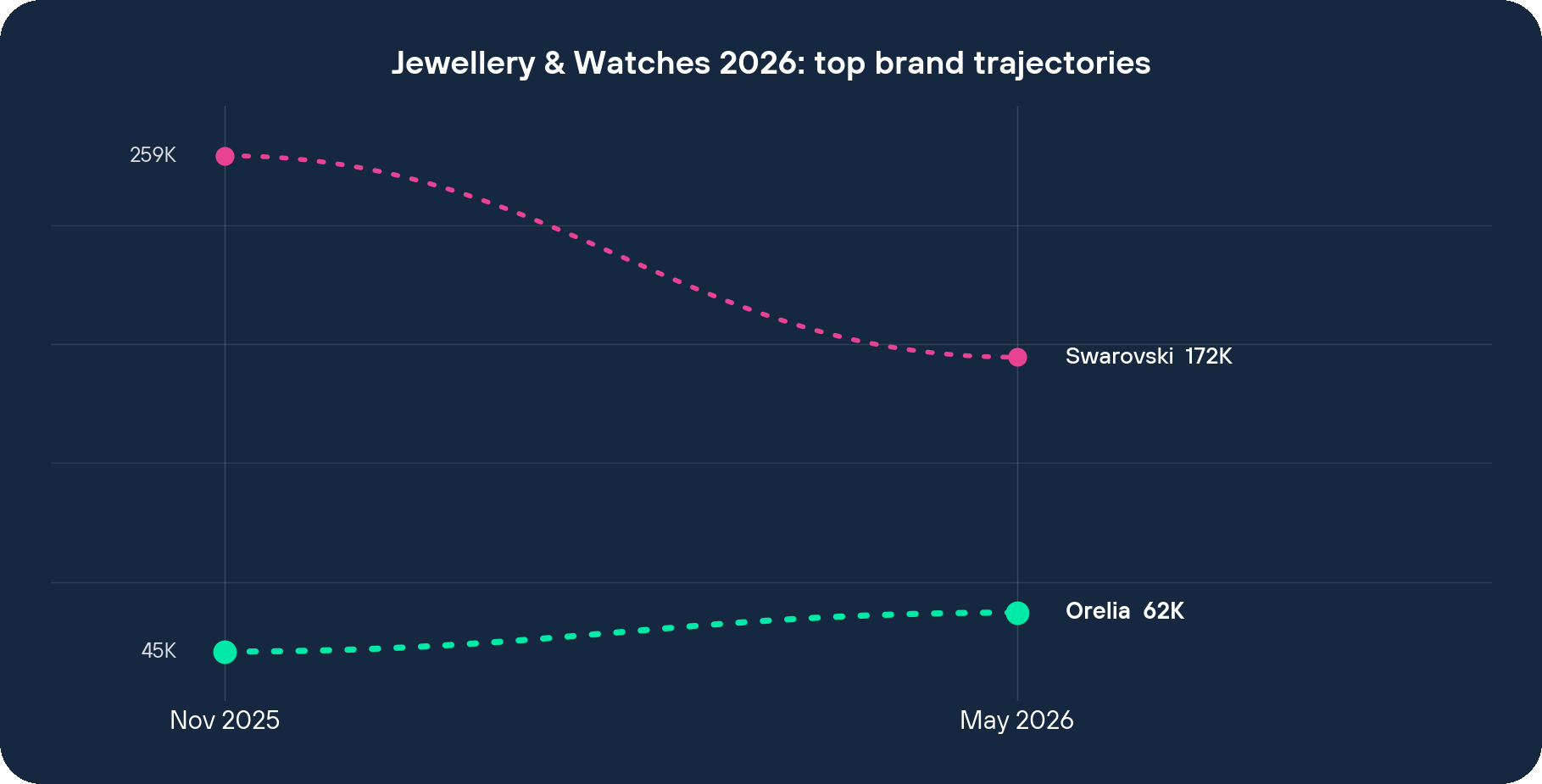

Across the 346 brands in this index, Orelia posted the single largest gain in real search share of anyone: +55.72 points, which is the gap between its own +37.79% and the market’s −17.94% over the period. In raw terms Orelia went from 44,655 monthly organic visits in November 2025 to 61,528 in May 2026, a gain of 16,873. That growth runs against the seasonal grain, which is what makes it notable. November is the seasonal peak for jewellery search because Christmas gifting pulls query volume up, and May sits close to the trough, so almost every brand in the table shows a November-to-May decline that is partly seasonal rather than structural. Orelia grew straight through that drag. Only four brands managed an absolute increase at all, Goldsmiths (+74,986, +23.68%), Beaverbrooks (+31,877, +6.72%), Orelia (+16,873, +37.79%) and Gemporia (+11,978, +17.01%), and of those four, Orelia has the least traffic and the largest real-share gain. Meanwhile the luxury and full-price names lost real share across the board: IWC −29.14, Breitling −25.61, Fossil −20.98, Swarovski −15.69, Cartier −15.08. Click below to access the latest Jewellery & Watches market report.

What Orelia has built on-site

Orelia’s catalogue structure makes the growth less surprising. The brand runs a programmatic set of product listing pages that crosses every product type by both style and material. Earrings exist as Gold Earrings, Silver Earrings, Pearl Earrings, Waterproof Earrings, Swarovski Earrings, Crystal Earrings, Emerald Earrings and Recycled Earrings, and the same crossing repeats for necklaces, bracelets and rings. On top of that sit gifting and personalisation pages targeting specific intent: personalised jewellery, initial pendants, zodiac pieces and birthstone jewellery. Each one is a landing page that answers a single query, and there are hundreds of them. Getting a page like that to rank is its own piece of work, covered in a guide to building jewellery product pages that rank.

The most telling choice is a top-level navigation category the traditional fine jewellers simply do not carry: Waterproof Jewellery, broken out into its own waterproof earrings, necklaces, bracelets and rings sub-pages. “Waterproof” describes how a customer wants to use the jewellery, wear it in the shower, at the gym, in the sea, every day, without it tarnishing, and it is a phrase people now type into Google. A jeweller whose site is organised around collections and hallmarked materials has no page that ranks for it. Orelia made it a headline category.

Two further decisions matter. Orelia treats “Swarovski crystal” as one material filter sitting alongside gold, silver, pearl, crystal and recycled, so a premium branded signifier becomes a checkbox. And it covers the full price-and-ethics spread inside one catalogue: an Orelia LUXE line reaches up-market, a Recycled Material range answers ethical-sourcing intent, and the entry price is kept deliberately low with a £40 free-delivery threshold, 15% off a first order, and student and keyworker discounts. A single site ranks for the everyday-wear buyer, the ethical buyer and the small-treat buyer at the same time.

Why that structure catches the search the market is shifting toward

The wider story in this report is a down-trade, organic demand moving out of luxury and full-price names and into affordable, pre-owned and lab-grown alternatives. When a shopper down-trades, their search behaviour changes in a way that matters here. They stop typing brand names they can no longer justify and start typing what they actually want: “waterproof gold earrings”, “recycled silver necklace”, “pearl bracelet”, “birthstone necklace for mum”. Those are non-branded, high-commercial-intent queries, and they map almost one-to-one onto Orelia’s product listing pages. A brand carrying a dedicated PLP for each of those searches, with relevant on-page copy and internal links pointing into it, is positioned to rank and win the visit. A brand whose catalogue is arranged around its own collections is not.

That is the part of Orelia’s growth this dataset can actually support. The pages exist, they target non-branded material and use-case queries, and non-branded search is exactly what grows when demand redistributes away from brand-led luxury. It explains a share of Orelia’s +37.79%; it does not account for all of it, and the honest reading treats it as a defensible portion rather than the whole.

Swarovski sells the same crystal and lost share

Swarovski is the clean comparison, because both brands sell crystal jewellery and they moved in opposite directions. Swarovski fell 33.63%, from 259,302 visits to 172,096, and lost 15.69 points of real share, while Orelia gained 55.72, a 71.41-point swing in six months between two competitors in the same category. Swarovski built its search identity on a single premium signifier, its own branded crystal, and a narrow, brand-led catalogue. Its homepage leads with “Masters of Light Since 1895”, shop-by-category tiles for necklaces, earrings and bracelets, and a stack of sale banners. That arrangement ranks well for “Swarovski necklace” and other branded queries, and it earns the brand’s considerable equity. Because the site is organised around Swarovski’s own collections, though, a generic “crystal earrings” or “recycled necklace” search finds no matching page. Orelia sells Swarovski’s own crystal as one filter among six, so it turns up in the broad affordable-jewellery search that a single-brand catalogue was never built to serve.

What this dataset can’t see

Honesty about the rest of Orelia’s number matters, because a single decision rarely explains six months of organic movement, and several drivers sit outside this table entirely. Orelia markets heavily on social and sells through third-party retailers as well as its own site, and both of those push branded search, people searching “Orelia” by name after seeing the product elsewhere, which lands as organic traffic that has nothing to do with category-page structure. The waterproof and everyday-gold trend is a market-wide demand shift Orelia rode rather than one it created on its own; that category grew for everyone selling into it. Orelia’s traffic is also small next to the giants, 61,528 visits against Pandora’s 1,780,571, and gaining real share is easier from a lower starting volume than from a large one. And this dataset does not split branded from non-branded traffic, so the category-page reading in the section above explains a portion of the gain and can be pushed no further than that.

What it means for a jewellery marketer

The practical point for anyone running search in this sector is straightforward. The part of Orelia’s gain we can measure came from holding a page for searches the incumbents left uncovered, durable everyday wear, specific materials, ethical sourcing, personalisation, at a time when Swarovski, with far more brand equity and budget, had no page for those queries. Those pages are cheap to build and they compound, because each one targets a query with buying intent that the brand-led catalogues structurally miss. Building that programmatic set of category and filter pages at scale is the core of ecommerce SEO for category pages. As demand keeps moving toward affordable, use-case-driven buying, the brands positioned to capture non-branded organic traffic are the ones that already have a landing page for each of those searches. Orelia’s category pages were in place ahead of that demand, and its November 2025 to May 2026 figures show it capturing a share the luxury names could not.

Want to see where your own brand landed? Download the full six-month dataset behind this analysis, then compare the same real-share and down-trade patterns across all Salience Index sector reports.

Further reading

- Salience Index gifting sector report, Jewellery sells heavily as a gift, so the gifting report shows how the same seasonal and gifting-intent demand behaves in an adjacent market.

- Wider jewellery search benchmarks, It sets out the broader organic search picture across the jewellery market that this Orelia breakdown sits inside.

- Bags and leather goods market report, Luxury accessories face the same down-trade in demand, so it helps a jewellery marketer see how the trend plays out beyond jewellery.