10

10  100

Brands Ranked

100

Brands Ranked 2026 UK Florist Market Analysis

UK flower search volume is down 7.3% since 2022. The industry visibility figure shows a modest +3% year on year, which sounds stable until you look at who got that growth and who didn’t.

This is not a market growing together. It’s a market in redistribution — and the redistribution is not subtle.

Arena Flowers grew 114%. Bunches grew 106%. J Parkers grew 72%. Meanwhile Floom lost 69%, Grace and Thorn lost 74%, and Sarah Raven — one of the most recognisable names in UK gardening and floristry — lost 25%. Same market. Same twelve months. The gap between the top grower and the biggest faller is 188 percentage points.

That matters because the florist market is now being shaped by a mix of changing search behaviour, stronger local and occasion intent, and a search landscape where authority and trust carry more weight than they did a year ago. The driver isn’t delivery speed. Same-day delivery keywords fell 17.8% since 2022. When every serious operator offers next-day delivery, the delivery promise stops differentiating. It becomes table stakes — the thing you assume before you even look.

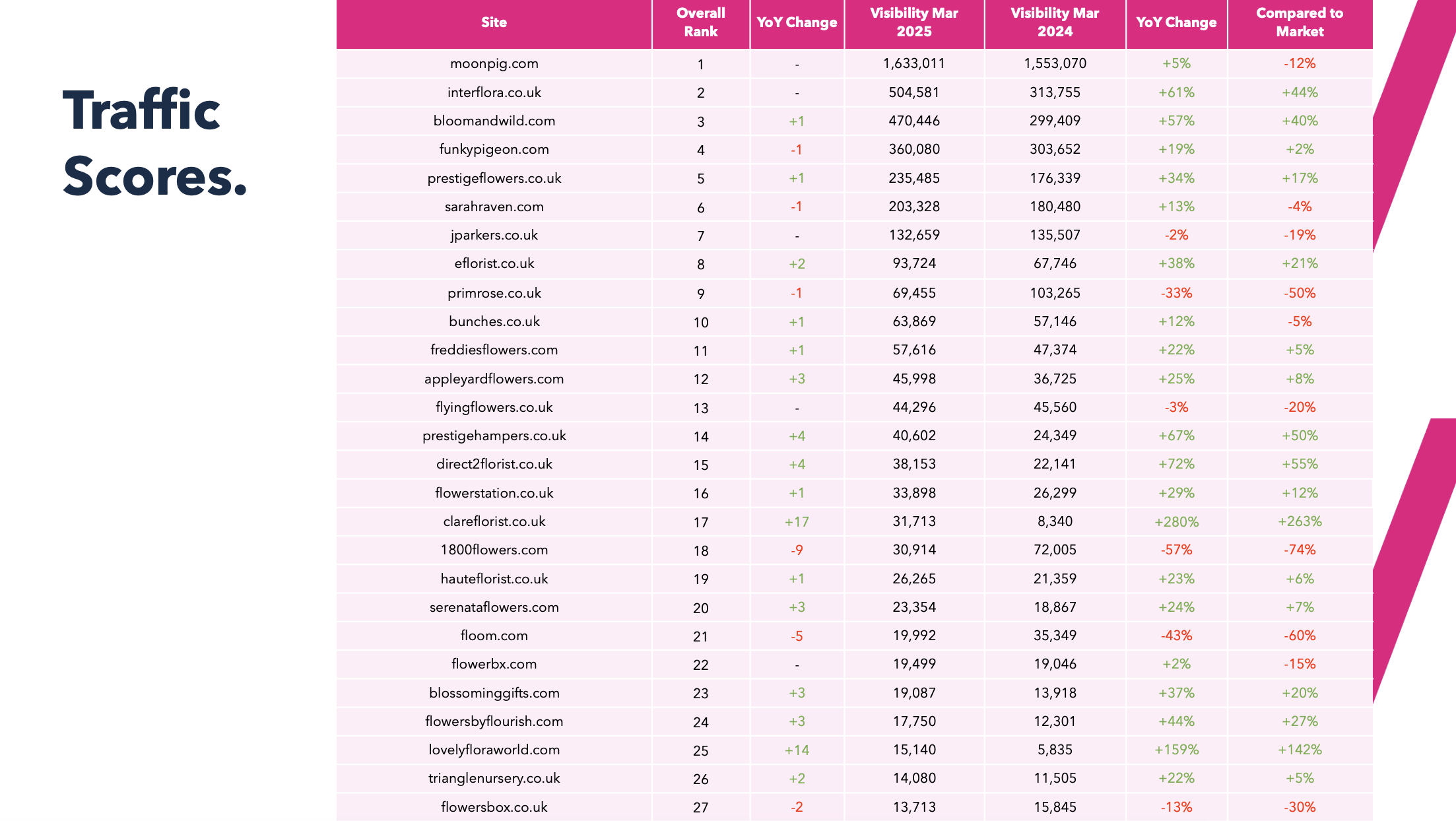

Which florist brands have the strongest organic visibility in 2026?

| Brand | 2026 Rank | Visibility Jan 2026 | Visibility Jan 2025 | YoY Change |

|---|---|---|---|---|

| Moonpig | 1 | 1,523,195 | 1,654,902 | -8% |

| Bloom & Wild | 2 | 604,476 | 499,412 | +21% |

| Interflora | 3 | 444,016 | 460,272 | -4% |

| Funky Pigeon | 4 | 288,623 | 294,150 | -2% |

| Prestige Flowers | 5 | 278,226 | 229,303 | +21% |

| J Parkers | 6 | 198,961 | 115,556 | +72% |

| Sarah Raven | 7 | 158,283 | 211,745 | -25% |

| Bunches | 8 | 130,493 | 63,229 | +106% |

| David Austin Roses | 9 | 122,286 | 104,346 | +17% |

| Eflorist | 10 | 121,342 | 106,845 | +14% |

| Appleyard Flowers | 12 | 83,699 | 65,143 | +28% |

| Direct2Florist | 14 | 73,622 | 43,794 | +68% |

| Flying Flowers | 15 | 60,753 | 43,150 | +41% |

| Arena Flowers | 20 | 28,921 | 13,491 | +114% |

A second group tells you just as much about where the market is heading. Flowercard rose 55%. Triangle Nursery climbed 48%. Freddie’s Flowers grew 36%. At the other end, Primrose dropped 46%, Flower Station fell 49%, and Floom was down 69%.

What this tells you is that scale alone is not keeping brands safe. The old assumption was that household names would keep winning generic demand because they had the broadest reach. That still helps, but it is no longer enough on its own. Weak pages, thin trust signals, and vague intent matching are getting exposed faster than they used to.

What are people actually searching for right now?

The keyword picture is the clearest signal of where intent is moving. Two behaviours are running in parallel.

First, heavy demand still exists for broad transactional terms. “Flower delivery” gets 62,000 searches per month at a competitiveness score of 82. “Send flowers” gets 20,000. “Florist near me” gets 22,000. These are the big battleground terms. They still drive volume and shape category leadership.

But alongside that, something more specific is happening.

Emerging searches — growing fast:

| Keyword | Monthly searches | Trend |

|---|---|---|

| White roses | 110,000 | +24% |

| Flowers near me | 40,500 | +21% |

| Bouquet of lilies | 3,600 | +83% |

| Flower subscription gift | 390 | +115% |

| White mums | 110 | +284% |

| Dried blooms | 40 | +1,500% |

Receding searches — losing traction:

| Keyword | Monthly searches | Trend |

|---|---|---|

| Flower shop | 40,500 | -55% |

| Buy flowers online | 9,900 | -39% |

| Order bouquet online | 9,900 | -39% |

| Florist delivery Sunday | 1,900 | -45% |

The pattern is not random. Older ecommerce shorthand — “flower shop”, “buy flowers online”, “order bouquet online” — is fading. People are getting more exact. They’re looking for a flower type, an occasion, a gift format, a timing need, a nearby solution. Search is becoming a precise tool in a way it wasn’t two or three years ago.

That shift has direct consequences for content and category strategy. Generic head terms still matter, but they no longer tell the whole story of demand. The growth is happening at the edges of the category, where intent is sharper and the customer often already knows precisely what they want.

And there are opportunity clusters hiding in plain sight. “Birth flowers” — flowers associated with a person’s birth month — generates 21,000 monthly UK searches with a competition score of just 3. “Letterbox flowers” generates 19,000 searches at a competition score of 24. These are not niche terms. They’re underserved demand in a contracting market.

Are reviews and brand trust now deciding who wins florist search?

Consider the baseline: 98% of people read online reviews for local businesses before making a decision. 90% read reviews before visiting a business. 36% are more likely to use a business that responds to all its reviews.

In a high-stakes gifting category — where a dead bouquet ruins a wedding anniversary — these aren’t soft preference signals. They’re risk-reduction signals that influence the decision before the first click happens.

Here’s where the major players stand:

| Brand | Reviews | Score |

|---|---|---|

| Moonpig | 525,734 | 4.2★ |

| Funky Pigeon | 323,730 | 3.9★ |

| Serenata Flowers | 242,269 | 3.8★ |

| Interflora | 148,430 | 4.2★ |

| Prestige Flowers | 145,606 | 4.2★ |

| Flying Flowers | 64,404 | 4.4★ |

| Bloom & Wild | 68,352 | 4.6★ |

| Direct2Florist | 37,437 | 4.8★ |

| Prestige Flowers | 145,606 | 4.2★ |

| David Austin Roses | 9,418 | 4.8★ |

| Arena Flowers | 22,245 | 4.6★ |

| Bunches | 17,251 | 4.3★ |

There’s something important to note here. “Social” and “social proof” are not the same thing. BM Flowers has the standout owned social score in the sector at 5,255 — significantly ahead of everyone else. That doesn’t put it near the top of the visibility leaderboard.

Arena Flowers, by contrast, has a much smaller social footprint. A social score of 135. A brand awareness rank of 18th in the sector. And yet Arena posted one of the sharpest visibility gains of the year.

The market is rewarding trust, not attention.

What the Arena Flowers rise says about where this is going

Arena Flowers is the case study that crystallises the whole picture — and the most interesting number in their data isn’t the one you’d expect.

Their branded search trend is down 25%.

Their organic visibility is up 114%.

They moved from Rank 32 to Rank 20 — a 12-place climb. Visibility grew from 13,491 to 28,921. They have 6,600 monthly brand searches and a brand awareness rank of 18th. Moonpig has 1,000,000 brand searches. Arena grew faster.

The visibility surge is clearly not being driven by a spike in branded demand. Nor is it being driven by overwhelming social reach. What it’s being driven by is a review profile — 22,245 reviews at 4.6 stars — that is converting generic discovery into performance.

Social proof in this market is doing more than polishing reputation. It’s turning anonymous category intent into attributable clicks. Reviews help off-site trust signals. They influence click-through rate. They affect local prominence. They matter to users and to search engines. When 98% of people read reviews before buying, review quality stops being a support metric and starts behaving like a growth channel.

Arena didn’t need to become the loudest brand in floristry to post one of the sharpest gains in the sector. It needed to become more believable, more useful, and more trusted at the point where generic demand converts to a click. In 2026, that looks like one of the smartest bets a florist can make.

Final take: which brands look set up for the next phase?

The leaders are no longer just the biggest names. They’re the brands whose visibility, trust, and query match are moving in the same direction.

Bloom & Wild, Bunches, J Parkers, Direct2Florist, Appleyard Flowers, and Arena Flowers all show forward momentum — though for different reasons. Moonpig, Interflora, and Funky Pigeon still have scale, but scale is not protecting every position as cleanly as it once did. Brands with weaker trust, weaker content fit, or weaker query coverage are finding out fast that market growth doesn’t lift everyone equally.

The strategic implication is clear enough. The opportunity isn’t just to rank more. It’s to be believed more. That means stronger category coverage, better product pages, more visible review equity, and a site experience that removes doubt instead of adding it. In a market where only 0.63% of Google searchers click to page two, the margin between being credible and being forgettable is thin.

Visibility is still shaped by search. But trust is now doing more of the earning.

This is the 2026 Florists Salience Index. 40 pages of search data on 100+ UK flower brands — visibility, authority, brand awareness, social, and 9,753 keywords tracked from 2022 to 2025. Free. No email gate.